Credit card fraud costs merchants far more than the stolen transaction amount. Between chargebacks, lost merchandise, processor fees, and the operational drain of fighting disputes, a single fraudulent order can wipe out the profit from dozens of legitimate sales.

The frustrating part? Most fraud is preventable with the right combination of payment authentication, detection tools, and response protocols. This guide covers the fraud types targeting your business, the prevention tactics that actually work, and what to do when fraud slips through anyway.

What Is Credit Card Fraud for Merchants?

Merchants prevent credit card fraud by combining strict payment policies with fraud-detection technology. For in-person sales, EMV chip readers block most counterfeit card attempts. For online sales, Address Verification Systems (AVS) and 3D Secure authentication stop unauthorized transactions and shift chargeback liability to the issuing bank.

Credit card fraud, from a merchant’s perspective, is any transaction where someone uses card data without the cardholder’s authorization. You shipped the product or delivered the service, but the cardholder never approved the purchase. When that cardholder disputes the charge, you lose the revenue, the merchandise, and pay a chargeback fee on top.

However, as security measures tighten, eCommerce fraud tactics continue to evolve. According to the Merchant Risk Council (MRC) 2026 Global eCommerce Payments and Fraud Report, global merchants lose an average of 3.2% of their total annual eCommerce revenue directly to payment fraud.

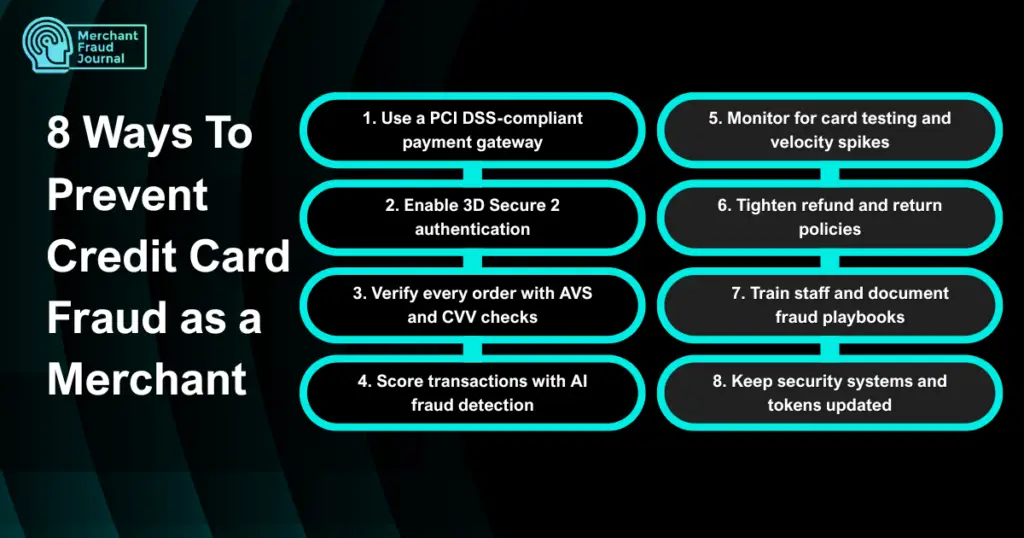

How To Prevent Credit Card Fraud as a Merchant

Each tactic below addresses a specific vulnerability in your payment flow. Layering multiple defenses creates stronger protection than relying on any single tool.

1. Use a PCI DSS compliant payment gateway

PCI DSS (Payment Card Industry Data Security Standard) is the baseline security requirement for handling card data. Rather than storing sensitive card information yourself, use a compliant gateway that tokenizes payment data. Verify your provider’s compliance status; it’s your first line of defense against data breaches.

2. Enable 3D Secure 2 authentication

3D Secure 2 (branded as Visa Secure or Mastercard Identity Check) adds a verification step during checkout. The cardholder’s bank authenticates the transaction, and if fraud still occurs, liability shifts to the issuing bank. The newer 2.0 version uses risk-based authentication, so low-risk transactions pass through without extra friction.

3. Verify every order with AVS and CVV checks

AVS compares the billing address entered at checkout against the address on file with the card issuer. CVV (Card Verification Value) confirms the buyer has the physical card in hand. Mismatches may signal various types of fraud. Consider declining or manually reviewing orders with address or CVV discrepancies.

4. Score transactions with AI fraud detection

Risk scoring analyzes signals like device fingerprint, IP (Internet Protocol) geolocation, purchase velocity, and behavioral patterns to flag suspicious orders. AI-powered tools learn from historical fraud patterns and can run pre-authorization or post-purchase, catching fraud before you ship. Platforms like Chargeflow analyze transactions using data from 15,000+ merchants, identifying repeat offenders across stores.

5. Monitor for card testing and velocity spikes

Set velocity thresholds or limits on how many transaction attempts a single IP, device, or card number can make within a short window. When bots test stolen cards, they trigger velocity limits. Auto-block or queue for review when thresholds are exceeded.

6. Tighten refund and return policies

Clear, documented policies displayed at checkout reduce disputes. Require proof of return receipt before issuing refunds. Make your policies specific enough that you can reference them as evidence if a chargeback occurs.

7. Train staff and document fraud playbooks

Your team is often the last line of defense. Train employees to recognize red flags: mismatched shipping and billing addresses, unusually large first-time orders, rush shipping requests on expensive items. Document escalation procedures so everyone knows what to do when something looks off.

8. Keep security systems and tokens updated

Regular software updates, payment plugin patches, and rotating API keys close vulnerabilities before fraudsters exploit them. Tokenization, replacing raw card data with non-sensitive tokens, means even if your system is breached, there’s nothing valuable to steal.

Take Control of Your Revenue Protection

Preventing credit card fraud isn’t about eliminating every single ounce of risk. Instead, it is about building a resilient system that deters bad actors while keeping checkout seamless for your legitimate customers. Fraudsters always look for the path of least resistance. Implementing these defenses ensures your business is no longer an easy target, allowing you to protect your hard-earned revenue and focus on growth.

Frequently Asked Questions

What is the best way for merchants to prevent credit card fraud?

A layered approach works best, combining payment authentication (3D Secure, AVS, CVV), AI-powered fraud detection, and chargeback alerts provides the strongest protection against both third-party fraud and friendly fraud.

What is the 2/3/4 rule for credit cards?

The 2/3/4 rule refers to Visa's Compelling Evidence 3.0 requirements, matching specific data points (like device ID, IP address, or shipping address) from prior undisputed transactions to defeat friendly fraud claims.

How can small merchants prevent credit card fraud without hurting checkout conversion?

Frictionless tools like 3D Secure 2 use risk-based authentication, low-risk transactions pass through without extra steps. Post-purchase fraud review also catches fraud without adding checkout friction, since the analysis happens after the order is placed but before you ship.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.