Merchant fraud protection is the combination of tools, strategies, and processes businesses use to identify fraudulent transactions, prevent chargebacks, and recover revenue when disputes occur. It covers everything from pre-checkout fraud screening to post-transaction dispute automation.

For eCommerce merchants, fraud isn’t just a security problem; it’s a margin killer. Between lost merchandise, chargeback fees, and the operational drain of manual dispute management, a single fraudulent transaction can cost 2-3x the original order value. Below, we break down how merchant fraud works, the most common threats targeting online businesses, and the layered defense strategies that actually protect revenue at scale.

What Is Merchant Fraud Protection?

Merchant fraud protection refers to the layered defense systems and strategies businesses use to detect, prevent, and respond to fraudulent activities like unauthorized credit card usage, friendly fraud, and identity theft. It safeguards revenue, prevents costly chargebacks, and builds customer trust.

Effective protection combines pre-transaction screening, real-time monitoring, and post-transaction dispute management, working together. The goal isn’t just stopping bad transactions, but also recovering revenue when eCommerce fraud slips through and keeping your chargeback ratio low enough to maintain healthy processor relationships.

Merchant fraud definition and classifications

Any deceptive activity targeting businesses during payment transactions fits the definition of merchant fraud. Fraud protection for merchants must account for criminals who use stolen cards, customers who dispute legitimate purchases, and bad actors who exploit return policies.

The first step to establishing a fool-proof merchant fraud protection is understanding what it is and how it works. First, you need to know that there’s a difference between fraud committed against merchants versus fraud committed by merchants. These are the classifications of merchant fraud:

- First-party fraud: A customer disputes a legitimate purchase, often called friendly fraud or chargeback abuse

- Third-party fraud: A criminal uses stolen payment credentials to make unauthorized purchases

- Merchant-initiated fraud: Bad actors posing as legitimate businesses to commit identity theft or launder money

Fraudsters constantly refine their methods, blending first-party and third-party deceptive practices into sophisticated digital schemes. Recognizing the mechanics behind the most common types of eCommerce merchant fraud allows online businesses to deploy targeted defenses and stop malicious transactions before they impact the bottom line.

How merchant fraud transpires

Examining how a deceptive claim unfolds from the merchant’s perspective reveals the critical touchpoints where revenue is put at risk. Here’s how various types of fraud typically unfold from the merchant’s perspective:

- Transaction occurs: A fraudulent purchase is made on your site using stolen credentials or an abusive customer profile.

Dispute filed: The true cardholder or a dishonest buyer contacts their issuing bank to formally contest the charge. - Chargeback issued: Funds are immediately reversed from your merchant account, and you are penalized with an additional administrative fee.

- Evidence window: You receive a strict timeline, typically 7 to 30 days depending on the card network, to submit compelling proof of delivery.

- Resolution: The bank evaluates the documentation to decide the final outcome, either returning the funds to you or closing the case permanently in favor of the claimant.

Losing individual transaction revenue is only the first wave of damage these deceptive claims cause. Card networks like Visa and Mastercard continuously monitor your dispute ratios to ensure network integrity. Exceeding their acceptable thresholds lands your business in punitive monitoring programs like VAMP or ECM, resulting in heavy fines, inflated processing fees, and the catastrophic loss of your merchant account.

How Merchant Fraud Hurts Your Business

The consequences of online deception touch every corner of a retail operation, far exceeding the initial value of a compromised transaction. Merchant fraud drains your resources. Here’s how you can contextualize the hidden expenses that threaten your business’s financial health.

- Direct revenue loss: Your business permanently loses the original transaction amount alongside the physical inventory and fulfillment costs.

- Escalating chargeback fees: Payment processors penalize merchants between $15 and $100 per dispute regardless of whether you win the case, and global losses from card-not-present fraud alone are expected to hit online sellers with $28.1 billion in annual damages.

- Accelerating global merchant losses: Cybercriminals show no signs of slowing down, indicating that global eCommerce fraud losses may reach $107 billion by 2029.

- The hidden cost multiplier: Dealing with fraud requires a substantial financial buffer because online merchants lose an average of $4.61 for every single dollar of successful fraud once chargeback fees, legal overhead, and legal penalties are factored in.

- Monitoring program penalties: Exceeding the strict dispute thresholds established by major networks like Visa or Mastercard pushes your business into high-risk monitoring programs that bring heavy operational fines.

- Operational resources drain: Employees spend valuable working hours compiling transaction evidence, tracing delivery records, and manually reviewing flagged accounts rather than focusing on growth.

A single dispute routinely costs a business more than double the original purchase price when factoring in fees and operational overhead. These immediate processing penalties represent only the opening wave of a much larger financial threat to your enterprise. Left unmanaged, these compound liabilities severely choke cash flow, degrade your merchant processing reputation, and ultimately jeopardize your capability to accept digital payments entirely.

Fraud Detection Vs. Fraud Prevention Vs. Fraud Protection

Fraud detection, prevention, and protection are often used interchangeably, but they mean different things. Deploying a comprehensive strategy requires understanding how each layer targets a distinct stage of the transaction lifecycle.

Integrating merchant fraud prevention, protection, and detection together creates a resilient, multi-layered defense system capable of neutralizing threats before they damage your bottom line. Here’s an overview of how these three layers differ from each other.

| Term | Definition | When it happens | Example |

|---|---|---|---|

| Fraud detection | Identifying suspicious activity | During or after transaction | Risk scoring flags unusual purchase pattern |

| Fraud prevention | Stopping fraud before it occurs | Before transaction completes | Blocking a known bad actor at checkout |

| Fraud protection | Full-cycle defense including recovery | Before, during, and after | Prevention + alerts + chargeback automation |

Detection tells you something’s wrong. Prevention stops it from happening. Protection covers the entire lifecycle, including winning back revenue when disputes occur. Most merchants focus heavily on detection and prevention while neglecting the recovery side, which is a mistake when friendly fraud now accounts for a significant portion of all chargebacks.

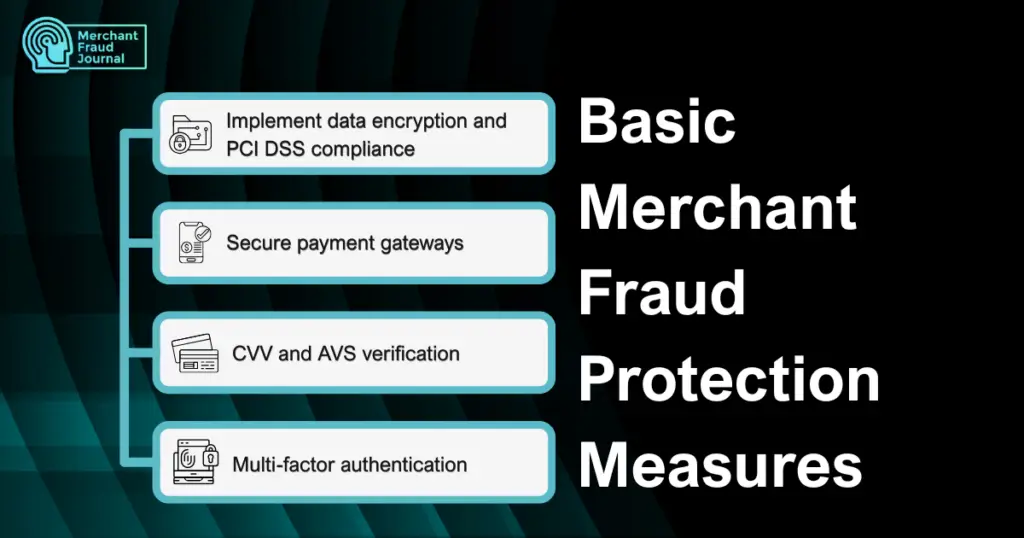

4 Basic Merchant Fraud Protection Measures

Fraud protection for merchants goes beyond luck or manual transaction reviews, which are no longer viable in today’s sophisticated threat landscape. The following essential security protocols provide your digital storefront with an automated first line of defense to block standard cyber threats immediately.

1. Implement data encryption and PCI DSS compliance

PCI DSS (Payment Card Industry Data Security Standard) is the baseline security standard for handling card data. Compliance isn’t optional as it is required by the card networks. Encryption protects data at rest (stored) and in transit (moving between systems). AES-256 encryption and TLS/SSL protocols are the current standards.

2. Secure payment gateways

A PCI-compliant payment gateway is your first line of defense. It handles sensitive card data so you don’t have to store it yourself, reducing your liability and attack surface. Look for gateways that offer tokenization as part of your broader fraud prevention for business strategy, replacing card numbers with non-sensitive tokens that are useless if stolen.

3. CVV and AVS verification

CVV (card verification value) is the 3-4 digit code on the card. AVS (address verification system) checks if the billing address matches what the card issuer has on file. Neither is foolproof, but they add friction for fraudsters while being low-friction for legitimate customers.

4. Multi-factor authentication

MFA (multi-factor authentication) adds a second verification step beyond passwords, typically a code sent to a phone or email. For customers, MFA prevents account takeover. For your team, it protects against internal breaches and social engineering attacks.

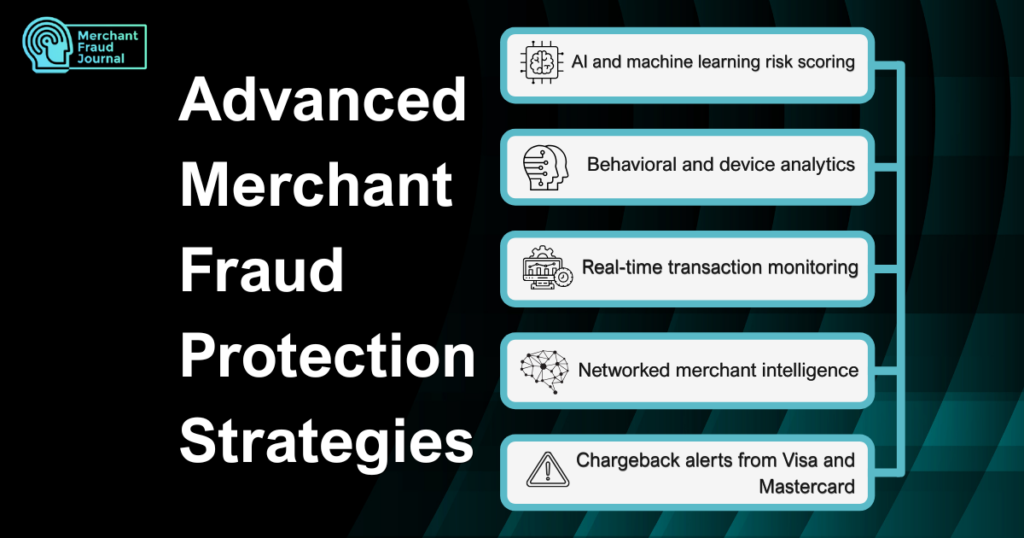

5 Advanced Merchant Fraud Protection Strategies

Once the basics are covered, more sophisticated approaches help you scale protection without scaling manual review. Standard filters are no longer enough to counter the automated tools utilized by modern cybercriminals. Transitioning to dynamic, data-driven security measures allows your storefront to neutralize complex fraud rings in real time. Here are the modern fraud protection strategies you can consider:

1. AI and machine learning risk scoring

Artificial intelligence (e.g., generative AI) and ML (machine learning) models analyze hundreds of transaction signals in real-time to score risk. They learn from historical data and adapt to new fraud patterns faster than rule-based systems. The best models improve continuously as they see more transactions, platforms like Chargeflow, Chargeback, and Chargebacks911, analyze millions of past chargebacks to train models that identify high-risk patterns before they become disputes.

2. Behavioral and device analytics

Behavioral biometrics track how users interact with your site, typing patterns, mouse movements, scroll behavior. Device fingerprinting identifies the specific device making a purchase. These signals catch anomalies that static data checks miss.

3. Real-time transaction monitoring

Batch review (checking transactions hours or days later) is too slow. Real-time monitoring evaluates risk before you fulfill the order, giving you the chance to cancel or verify suspicious purchases. The window between order and fulfillment is your best opportunity to prevent fraud.

4. Networked merchant intelligence

Individual merchants see only their own fraud. Networks share signals across thousands of merchants about known bad actors, suspicious device fingerprints, behavioral patterns. When a fraudster hits one merchant in the network, every other merchant benefits from that intelligence.

5. Chargeback alerts from Visa and Mastercard

5 Best Practices to Reduce Fraud and Chargebacks

Deploying automated security systems provides an excellent baseline of protection, but technological tools achieve maximum efficiency only when paired with standardized internal operations. Establishing strict routines ensures you can systematically intercept high-risk orders and handle customer disputes with consistency. Here are the practices you should adopt to fortify your store’s defenses:

1. Monitor your chargeback ratio against VAMP and ECM thresholds

Visa’s VAMP program threshold is 0.9% of transactions, while Mastercard’s ECM threshold is 1.5%. Track your ratio in real-time, instead of just monthly. By the time you see a problem in monthly reports, you may already be in violation.

2. Layer pre-purchase and post-purchase fraud controls

No single tool catches everything. Combine pre-checkout fraud scoring with post-purchase verification and automated dispute management. Pre-purchase tools stop obvious fraud; post-purchase verification catches friendly fraud before fulfillment; dispute automation recovers revenue when chargebacks happen anyway.

3. Automate refunds for high-risk orders

Sometimes a proactive refund costs less than a chargeback. When alerts flag a dispute in progress, automatic refunds protect your ratio and avoid the dispute fee. Set rules based on transaction value and risk score.

4. Build compelling evidence for dispute recovery

Evidence quality determines win rates. You’ll want delivery confirmation, IP addresses, device fingerprints, customer communications, and proof of prior transactions. Automated evidence collection pulls data points from multiple sources to build stronger cases.

5. Update policies and train teams continuously

Preventing fraud in business starts with recognizing that fraud tactics evolve constantly. Clear refund policies reduce friendly fraud by setting expectations. Staff training helps identify red flags before orders ship.

How to Choose a Merchant Fraud Protection Solution

Selecting the right security partner requires a careful evaluation of how a software platform fits into your existing payment infrastructure. Identifying the core capabilities of a potential vendor ensures your business secures comprehensive coverage without introducing unnecessary friction to the checkout experience.

- Integration depth: One-click connectors sync seamlessly to your eCommerce platform, payment processor, and CRM (customer relationship management) system without extensive custom coding.

- Automation level: End-to-end automation handles high-volume tasks instantly, removing the need for slow, manual operational workflows.

- Evidence quality: Advanced data enrichment automatically gathers deep technical proof to generate compelling dispute responses.

- Network intelligence: Real-time access to cross-merchant fraud signals blocks known bad actors before they target your specific store.

- Pricing model: Performance-based pricing aligns vendor incentives with your success, offering an alternative to fixed flat fees that charge you regardless of results.

- Compliance adherence: Certified alignment with SOC 2 Type II, GDPR, and PCI DSS standards safeguards sensitive customer payment records.

- Full-cycle coverage: A unified platform manages prevention, real-time alerts, and recovery rather than forcing you to patch together multiple fragmented point solutions.

Choosing an inadequate security solution leaves critical gaps in your transaction workflow that cybercriminals will eventually exploit. Subscribing to a platform that lacks deep network intelligence or automated evidence generation severely limits your capability to fight back against rising dispute volumes. Investing in a robust, fully integrated system establishes a permanent shield that safeguards your enterprise revenue from the compounding damage of digital theft.

Leverage AI-Powered Fraud and Chargeback Protection

Waiting until fraud strikes is a costly mistake. Proactive tools that detect and block suspicious activity before a transaction is approved are your strongest line of defense. Comprehensive protection requires prevention, alerts, and automated recovery working together. Remember that safeguarding your revenue isn’t just about recovering losses; it’s about building a resilient system that makes your business a harder target from the start.

Frequently Asked Questions

What is the 10/80/10 rule for fraud?

The 10/80/10 rule suggests that roughly ten percent of people will always act honestly, ten percent will always attempt fraud if given the opportunity, and the remaining eighty percent could go either way depending on circumstances and controls in place.

What are the 6 pillars of fraud management?

The six pillars of fraud management typically include prevention, detection, investigation, resolution, analysis, and policy management. These elements represent the complete lifecycle of identifying, stopping, and learning from fraudulent activity.

How much does merchant fraud cost eCommerce businesses annually?

Merchant fraud costs eCommerce businesses billions globally each year when accounting for lost merchandise, chargeback fees, operational costs, and penalties from card network monitoring programs. Friendly fraud represents a growing share of total losses.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.