eCommerce merchant fraud is any activity in which bad actors commit theft against businesses by tampering with payment systems or deceiving operations. Unlike consumer fraud, where buyers get scammed, merchant fraud puts businesses on the losing end, absorbing chargebacks, losing inventory, and facing potential account termination.

This guide breaks down what merchant fraud is, the most common eCommerce fraud types targeting merchants, the warning signs that signal an attack, and the layered prevention strategies that actually work.

What Is eCommere Merchant Fraud?

eCommerce merchant fraud occurs when someone manipulates payment systems, poses as a legitimate business, or hijacks existing merchant accounts to steal funds, goods, or services. It targets businesses that accept payments, especially online retailers processing card-not-present transactions.

Examples of Merchant Fraud

Consider a fraudster who creates a fake eCommerce website selling luxury electronics at steep discounts. They register as a merchant with a payment processor using stolen or fabricated business credentials, then advertise heavily on social media to attract buyers. Customers enter their credit card details and purchase items that never arrive, while the fraudster collects the payments and disappears before chargebacks are filed.

In a more sophisticated variation, rather than building a fake storefront from scratch, the criminal obtains the login credentials of an established online retailer through a phishing attack or data breach and quietly redirects incoming payments to their own account. Because the hijacked merchant has a legitimate processing history, the fraud goes undetected longer, amplifying the financial damage to both customers and the genuine business owner.

Who Is Affected by eCommerce Fraud?

Any business accepting online payments faces exposure. eCommerce retailers selling physical goods often see triangulation fraud and friendly fraud. SaaS (software-as-a-service) and subscription companies deal with card testing and chargeback abuse. Marketplaces face unique challenges because they’re managing fraud risk across multiple sellers.

Digital goods sellers and high-ticket merchants tend to attract more sophisticated attacks. Fraudsters target digital products because there’s no shipping delay, so they get instant value. High-ticket items offer bigger payouts per successful fraud attempt.

What Is the Cost of eCommerce Merchant Fraud?

The financial damage runs deep. U.S. merchants now incur an average of $4.61 in total costs for every $1 of direct fraud loss when you factor in fees, operational overhead, and downstream effects. However, while monetary losses cover the overt consequences of merchant account fraud, there are also other underlying costs that business owners must take note of. Below are the types of merchant fraud costs:

- Direct costs: Lost merchandise, refund payouts, chargeback fees, and card network fines

- Indirect costs: Staff time investigating disputes, customer service burden, and potential merchant account termination

- Hidden costs: False declines blocking legitimate customers, lost lifetime value, and reputational damage

The most visible financial hits come from direct and indirect costs that accumulate with each fraudulent transaction. On the direct side, merchants absorb the loss of goods already shipped, issue refunds, and then face chargeback fees ranging from $20 to $100 per dispute, on top of any fines levied by card networks like Visa or Mastercard for excessive dispute ratios.

Indirect costs compound the damage behind the scenes. Every disputed transaction triggers an internal investigation, pulling staff away from revenue-generating work. Customer service teams field complaints, gather documentation, and manage communications, all of which add labor costs that never appear on a chargeback statement. .

Perhaps the most overlooked dimension of merchant fraud is the damage that never shows up in a dispute report. Overly aggressive eCom fraud filters, often tightened in response to attacks, end up declining your legitimate customers whose orders look suspicious by pattern alone.

Each false decline is a lost sale, but more importantly, it is a potential lifetime customer pushed toward a competitor. Repeated friction erodes trust, and word travels.

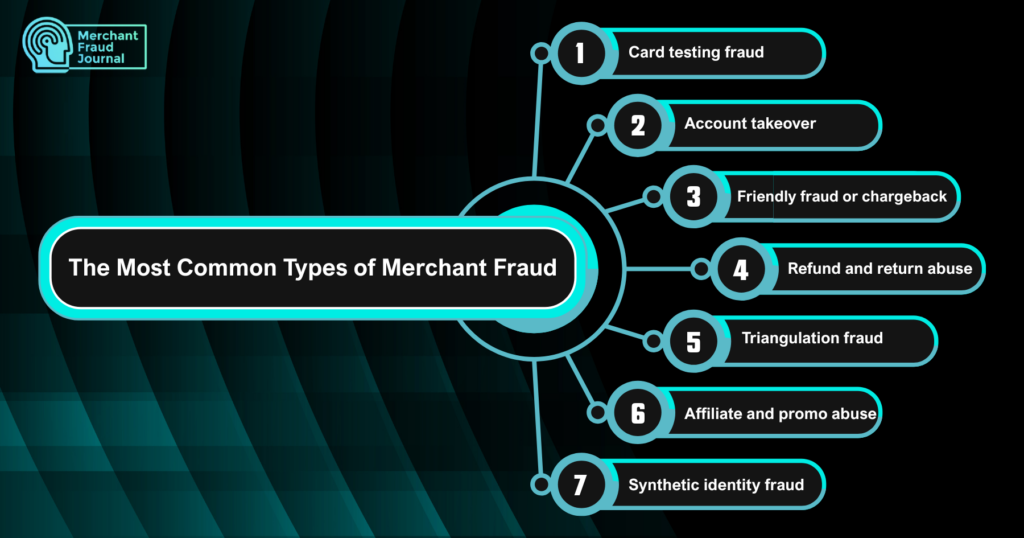

What Are The Most Common Types of eCommerce Merchant Fraud?

Merchant fraud takes many forms, and each type calls for a different detection and prevention approach. Left unchecked, even a single fraud vector can erode customer trust, inflate operational costs, and expose a business to significant financial liability. Here are the common types of eCommerce fraud merchants might encounter:

1. Card testing fraud

Fraudsters validate stolen card numbers by running small purchases, often under $5, before attempting larger transactions. You might see a sudden spike in low-value orders from unfamiliar customers, sometimes dozens within minutes. The goal is to confirm which cards work before selling them or making bigger purchases elsewhere.

2. Account takeover fraud

Account takeover (ATO) happens when criminals gain access to legitimate customer accounts through credential theft, phishing, or data breaches. Once inside, they use stored payment methods to make unauthorized purchases. The real customer often doesn’t notice until their statement arrives, and by then you’ve shipped the order and face a chargeback.

3. Friendly fraud or chargeback fraud

Friendly fraud or chargeback fraud occurs when customers dispute legitimate purchases to get refunds while keeping the merchandise. The term friendly refers to the customer appearing legitimate. They’re real people with valid cards, not criminals with stolen credentials.

This type often goes undetected because the transaction looks normal at checkout. It’s also notoriously difficult to prove, which is why win rates on friendly fraud disputes historically hover around 20–30% without proper evidence.

4. Refund and return abuse

Policy exploitation takes many forms: claiming items never arrived when they did, returning different or used items, or abusing return windows repeatedly. No chargeback gets filed, so it doesn’t hit your dispute ratio, but it still erodes margins. Serial abusers often operate across multiple merchants, making network-level intelligence valuable for identification.

5. Triangulation fraud

Triangulation fraud is a three-party scheme that works like this: a fraudster sets up a fake storefront, collects real customer payments for products at attractive prices, then uses stolen card credentials to fulfill orders from legitimate merchants. You ship the goods, the real cardholder disputes the charge, and you’re left with the chargeback. The fraudster keeps the customer’s payment.

6. Affiliate and promo abuse

Fraudsters exploit referral programs, discount codes, and promotional offers through fake account creation. They might harvest sign-up bonuses repeatedly, stack coupons in unintended ways, or generate fake referrals.

7. Synthetic identity fraud

Synthetic identities combine real and fabricated information, like a legitimate Social Security number paired with a fake name and address, to create new identities that pass initial verification. Fraudsters use synthetic identities to open merchant accounts, apply for credit, or make purchases that won’t be disputed by a real cardholder.

What Are the Warning Signs and Red Flags of Merchant Fraud?

Early detection relies on recognizing patterns before transactions complete or disputes escalate. No single indicator confirms fraud, but combinations of signals warrant closer review.

1. Mismatched billing and shipping addresses

AVS (address verification system) mismatches raise flags, especially when combined with expedited shipping requests. Fraudsters often ship to addresses different from the billing address because they don’t have access to the cardholder’s home.

2. Unusual order volumes and purchase velocity

Watch for both extremes: sudden spikes in orders and unusually large single purchases. Velocity checks flag multiple orders within short timeframes from the same customer, device, or IP (Internet Protocol) address. Legitimate customers rarely place five orders in ten minutes.

3. Repeated card declines and CVV failures

Multiple failed authorization attempts signal card testing or stolen card use. Real customers occasionally mistype their CVV (card verification value) once, but they don’t fail it four times in a row while trying different numbers.

4. High-risk IP and device signals

Geolocation mismatches between IP address and billing address raise concerns. VPN (virtual private network) and proxy use, device fingerprint anomalies, and connections from known merchant services fraud hotspots all contribute to risk scoring.

5. Suspicious refund and dispute patterns

Customers with abnormally high return rates, serial dispute filers, and patterns suggesting policy abuse often appear normal on individual transactions. Identifying them requires historical data analysis across your customer base, or access to network-level data showing their behavior across other merchants.

How to Detect eCommerce Merchant Fraud

Detection bridges the gap between recognizing warning signs and taking action. The accuracy of your detection depends heavily on data breadth. Single-merchant data has blind spots that network-level intelligence fills.

- Rule-based screening: Static rules flag transactions matching known fraud patterns

- ML (machine learning) scoring: ML models analyze hundreds of data points per transaction to assign risk scores in real time

- Network intelligence: Cross-merchant data sharing identifies repeat offenders that single-merchant data misses

- Behavioral analytics: Session and interaction patterns reveal anomalies like copy-pasted form fields or bot-like behavior

The most effective detection combines all four approaches. Rules catch obvious patterns, ML handles nuance, network data exposes serial abusers, and behavioral analytics flags suspicious sessions before checkout completes.

How to Prevent eCommerce Merchant Fraud

Prevention works best as a layered strategy combining authentication, technology, and operational processes. Equally important is cultivating a security-aware culture where employees are trained to recognize and report threats before they escalate. Here are fraud prevention tips to consider:

1. Strengthen authentication with CVV, AVS, and 3DS

Each authentication layer adds friction for fraudsters while providing evidence for disputes. CVV confirms the person has physical access to the card. AVS matches the billing address against the card issuer records. 3D Secure adds a cardholder authentication step and can shift liability to the issuer for authenticated transactions.

2. Deploy machine learning risk scoring

ML models analyze transaction attributes, such as device fingerprint, behavioral signals, purchase history, and network data, to assign risk scores in milliseconds. The models improve continuously as they process more transactions and receive feedback on outcomes.

3. Use post-purchase fraud screening

Screening orders after checkout but before fulfillment catches merchant account fraud that slipped through pre-authorization checks. This window allows you to cancel, verify, or flag risky orders before shipping merchandise you won’t recover.

4. Activate real-time chargeback alerts

Alert networks from Visa (Verifi) and Mastercard (Ethoca) notify you of incoming disputes before they become chargebacks. You can issue preemptive refunds to avoid the chargeback entirely, protecting your dispute ratio and saving the chargeback fee.

5. Automate dispute evidence and recovery

Manual dispute processes miss deadlines and lack consistency. Automated evidence collection pulls data from your payment processor, eCommerce platform, shipping provider, and customer communications to build compelling responses.

6. Monitor dispute ratios and card network thresholds

Visa’s VAMP (Visa Acquirer Monitoring Program) and Mastercard’s ECM (Excessive Chargeback Merchant) program impose penalties when you exceed thresholds, typically 0.9% dispute ratio or 100 disputes monthly. Consequences include fines, reserve requirements, and potential account termination.

Merchant Fraud Is Evolving

As technology continues to advance, so is the fraud landscape. AI-powered fraud attacks use deepfakes to bypass identity verification and generate convincing phishing content at scale. BNPL (buy now, pay later) fraud schemes exploit the gap between purchase and payment. Cross-border transactions face jurisdictional challenges in dispute resolution. With this rapid evolution, eCommerce merchants especially, must grow their understanding of merchant fraud through regular updates and continuous learning.

Frequently Asked Questions

What are the 4Ps of fraud?

The 4Ps of fraud are pressure (financial or personal motivation driving the fraudster), perceived opportunity (weak controls that make fraud possible), post-hoc rationalization (how fraudsters justify their actions), and prevention failure (systemic gaps that allowed the fraud to occur).

What are the five requirements for fraud?

The five legal elements to prove fraud are: a false statement of material fact, knowledge that the statement was false, intent to deceive the victim, justifiable reliance by the victim on the false statement, and resulting damages or injury.

Is merchant fraud the same as chargeback fraud?

Chargeback fraud is one type of merchant fraud where customers dispute legitimate purchases to obtain refunds while keeping merchandise. It's also called friendly fraud and represents one of the most common forms of merchant services scams today.

Who is liable when merchant fraud happens?

In most card-not-present transactions, the merchant bears liability for fraudulent charges. Liability can shift to the card issuer when merchants use authentication methods like 3D Secure, or when merchants successfully dispute chargebacks with compelling evidence.

Can small businesses afford merchant fraud prevention?

Many fraud prevention and chargeback management solutions offer usage-based pricing with no upfront costs or minimums. Success-based models mean you only pay for chargebacks recovered, making protection accessible to businesses of all sizes.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.