Fraudsters no longer need technical skills to run sophisticated attacks. With generative artificial intelligence (AI) tools, a single bad actor can launch thousands of synthetic identity schemes, phishing campaigns, and automated card tests simultaneously. All these can take place while adapting in real time to dodge your defenses.

This guide breaks down how criminals weaponize AI against eCommerce merchants, and the layered defense strategies that actually work to prevent chargebacks before they happen.

What Is AI-powered eCommerce Fraud?

Fraudsters use AI to scale, automate, and disguise malicious actions, blending attacks seamlessly into the flow of legitimate eCommerce transactions. Instead of slow, manual schemes, bad actors now leverage machine learning and generative AI to bypass traditional rule-based security at speeds that weren’t possible even two years ago.

So what makes AI-powered eCommerce fraud different from the old-school stuff? Three things: scale, adaptability, and quality. A single fraudster can now run thousands of attacks simultaneously. According to Group-IB’s 2026 research, AI-powered scam operations combine synthetic voices, large language models LLM-driven coaching, and automated responders to run fully autonomous fraud at scale. This is a level of reach that was operationally impossible for individual actors just a few years ago.

Why Fraudsters Are Turning to AI

The economics of fraud have shifted dramatically. AI makes attacks faster, cheaper, and more profitable than manual methods ever were. Generative AI-enabled fraud surged 1,210% in 2025 alone. That growth rate is not a rounding error. It reflects a structural change in how fraud operations are built and scaled.

- Lower barrier to entry: Accessible AI tools require no technical expertise, so amateur fraudsters can execute sophisticated schemes

- Unprecedented scale: Automated systems run thousands of attacks simultaneously across multiple merchants

- Higher success rates: AI-generated content bypasses filters designed to catch human-written fraud attempts

- Reduced detection risk: Adaptive attacks learn from failures and adjust tactics in real time

What once required organized crime rings now takes a single bad actor with the right tools. The rise of fraud-as-a-service platforms has lowered the barrier further, giving even low-skill threat actors access to sophisticated attack infrastructure on demand. The technologies driving AI-powered fraud include LLMs that generate realistic text, deepfake tools that fabricate identities, and autonomous bots that learn from failed attempts.

How Fraudsters Use AI to Commit eCommerce Fraud

According to Veriff’s Fraud Industry Pulse Survey 2026, 75% of respondents specifically cited more AI-driven fraud attacks, with 78% expecting the threat to grow further. Meanwhile, AI-facilitated fraud losses are projected to grow from $12.3 billion in 2023 to $40 billion by 2027, a 32% compound annual growth rate.

Understanding specific attack methods helps you recognize these vulnerabilities in your own operations. Here’s what’s actually happening out there.

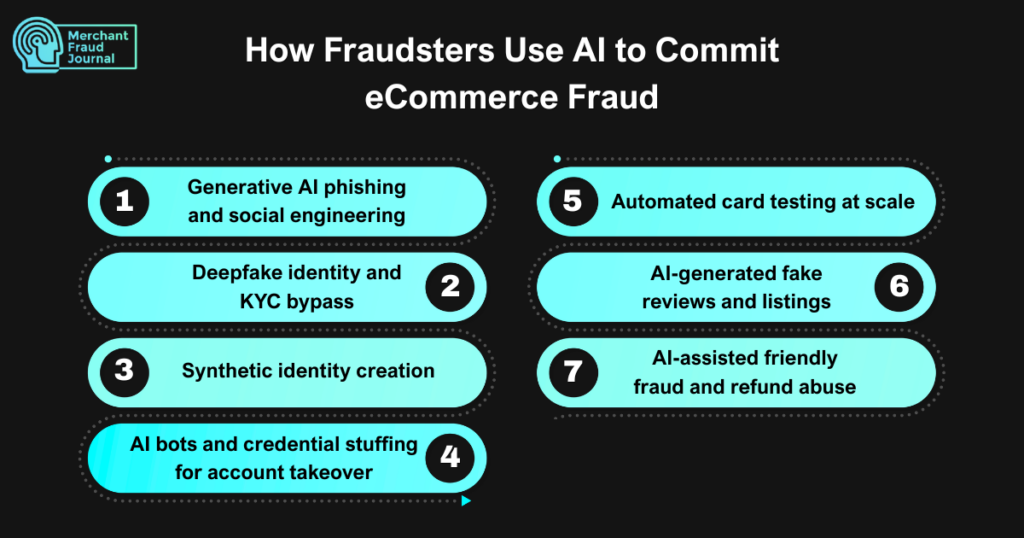

1. Generative AI phishing and social engineering

LLMs craft convincing phishing emails, chat messages, and fake customer service interactions that lack the telltale grammar errors of traditional scams. Voice cloning technology enables vishing attacks where fraudsters impersonate real people over the phone (e.g., voice cloning using AI to mimic CEO’s voice).

Social engineering, which involves manipulating people into revealing sensitive information, becomes more effective when AI personalizes each message based on scraped data about the target. The days of spotting fraud by looking for typos are over.

2. Deepfake identity and KYC bypass

Fraudsters use AI-generated images and videos to pass identity verification checks that once stopped them cold. Know Your Customer (KYC) processes, which verify that customers are who they claim to be, struggle against synthetic faces and forged documents. Generative AI produces realistic driver’s licenses, passports, and utility bills in seconds. The quality improves constantly, and verification systems haven’t kept pace.

3. Synthetic identity creation

Synthetic identity fraud combines real data (like a stolen Social Security number) with fabricated details to create entirely fictional personas. AI generates realistic personal histories, credit profiles, and behavioral patterns that pass verification systems.

Here’s the tricky part: synthetic identities often age for months, building legitimate-looking transaction histories before executing large-scale fraud. By the time the scheme becomes obvious, the damage is done.

4. AI bots and credential stuffing for account takeover

AI-powered bots test stolen username and password combinations across hundreds of sites simultaneously. When they find a match, they’ve achieved account takeover (ATO); this provides full access to a legitimate customer’s account. Modern bots adapt to CAPTCHAs, mimic human mouse movements, and vary their timing to avoid detection. They’re remarkably good at looking human, which is exactly the point.

5. Automated card testing at scale

Before making large purchases, fraudsters validate stolen card numbers through small test transactions. AI bots run thousands of card tests per hour, quickly identifying which cards remain active. The downstream impact hits merchants hard. It could be in the form of chargebacks, processor flags, and potential placement in monitoring programs that come with fines and increased fees.

6. AI-generated fake reviews and listings

Generative AI creates convincing product reviews, fraudulent marketplace listings, and counterfeit storefronts. Bad actors use fake storefronts to deceive both platforms and buyers, enabling everything from selling nonexistent products to harvesting payment credentials. The content quality has reached a point where distinguishing AI-generated reviews from authentic ones requires specialized detection tools.

7. AI-assisted friendly fraud and refund abuse

Bad actors use AI to craft convincing false claims, identify merchant policy loopholes, and automate item not received or item not as described disputes. This isn’t traditional fraud; rather, it involves customers (or people posing as customers) exploiting the chargeback system. AI helps abusers write compelling dispute narratives and even generate fake evidence like doctored delivery photos. The result? More chargebacks that are harder to fight.

How to Detect AI-Powered eCommerce Fraud

Unlike rule-based filters that react to known patterns, AI-powered detection continuously learns from new data, recognizing the subtle behavioral signals that separate legitimate shoppers from sophisticated bots and fraudsters. Fighting AI requires AI. Here’s how modern detection systems identify threats that slip past traditional defenses.

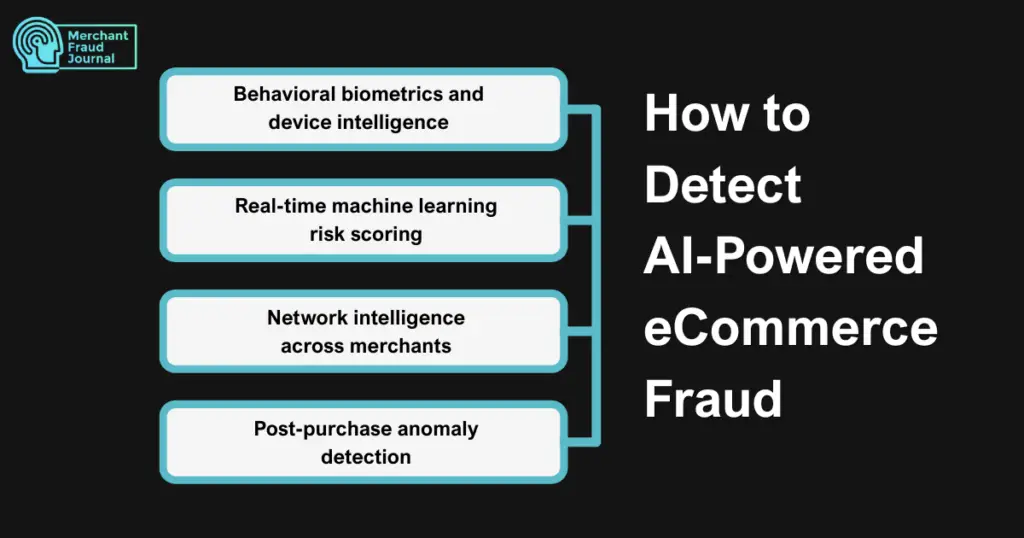

1. Behavioral biometrics and device intelligence

Typing patterns, mouse movements, device fingerprints, and session behavior reveal whether a user is human and whether they are the legitimate account holder. Strong Customer Authentication (SCA) adds a critical verification layer, ensuring that even when credentials appear valid, identity is confirmed through multiple factors before access is granted. Even when credentials are valid, behavioral signals expose bots and account takeover attempts.c

2. Real-time machine learning risk scoring

Machine learning models analyze transactions in milliseconds, assigning risk scores based on hundreds of data points. Unlike static rules, machine learning models learn from new attack patterns and adapt continuously. The difference is dramatic: rules catch known threats, while ML catches anomalies that don’t match any existing pattern.

3. Network intelligence across merchants

Shared data across merchant networks identifies repeat abusers, fraud rings, and known bad actors before they strike. When a fraudster burns one merchant, consortium data ensures they can’t simply move to the next.

4. Post-purchase anomaly detection

Monitoring doesn’t stop at checkout. Suspicious fulfillment addresses, unusual claim patterns, and return abuse indicators all surface after the transaction completes. Catching fraud before fulfillment prevents losses that would otherwise become chargebacks.

Staying ahead requires more than awareness; it demands continuous investment in detection tools, fraud prevention infrastructure, and team education. The fraudsters are iterating constantly, and your defenses need to do the same.

How to Stop AI-Driven eCommerce Fraud

The most resilient organizations treat security not as a checkpoint, but as a continuous discipline woven into every layer of their operations. Detection matters, but prevention delivers ROI. Here’s how to build a defense that actually works.

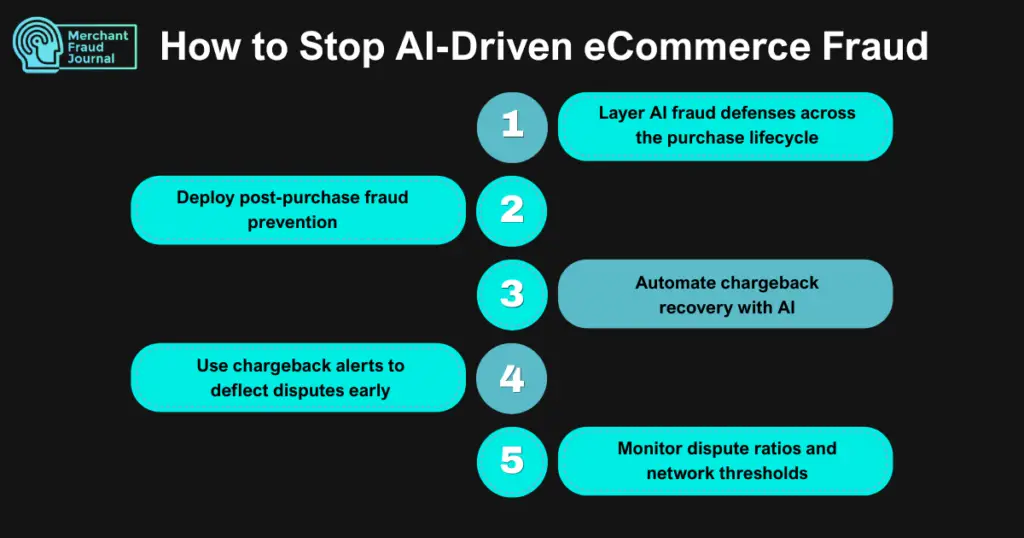

1. Layer AI fraud defenses across the purchase lifecycle

Pre-transaction, transaction, and post-transaction protection work together rather than as isolated point solutions. Gaps between systems create opportunities for sophisticated attackers. A unified approach including prevention, alerts, recovery, and analytics in one platform eliminates the blind spots that fragmented tools leave exposed.

2. Deploy post-purchase fraud prevention

Stopping fraud, especially among high-risk merchants, after checkout but before fulfillment prevents losses without adding friction to legitimate purchases. Order verification, risk scoring, and automated cancellation workflows catch threats that slip through checkout.

3. Use chargeback alerts to deflect disputes early

Real-time alerts from Visa and Mastercard let merchants refund transactions before disputes become chargebacks. Refunding early keeps your dispute ratio healthy and avoids the fees associated with formal chargebacks.

4. Automate chargeback recovery with AI

When chargebacks happen despite prevention efforts, AI-powered dispute response recovers revenue that would otherwise be lost. Evidence collection, compelling evidence assembly, and deadline management all run on autopilot.

5. Monitor dispute ratios and network thresholds

Tracking chargeback ratios in real time prevents nasty surprises when you’re suddenly placed in a monitoring program. Proactive alerts when approaching thresholds give you time to act.

A layered, automated defense that covers the full purchase lifecycle transforms a reactive scramble into a controlled, measurable program. For a deeper look at how to put these eCommerce fraud protections in place. Consider advanced tools and tactics that keep high-volume merchants protected without slowing down legitimate sales.

Stop AI-Driven Fraud Before It Impacts Your Bottomline

AI-driven fraud is evolving faster than most businesses can react, and the cost of a reactive posture shows up directly in chargebacks, lost inventory, and eroded customer trust. The good news is that the same AI capabilities fraudsters are weaponizing can be deployed in your defense.

Investing in a layered fraud prevention strategy, one that combines machine learning models, behavioral analytics, and real-time transaction scoring, shifts your position from target to fortified. The question is no longer whether AI-powered fraud will hit your store, but whether your defenses will be ready when it does.

Frequently Asked Questions

How does AI contribute to fraud?

AI enables fraudsters to automate attacks at scale, generate convincing fake identities and content, bypass security measures, and exploit merchant policies faster than manual methods ever allowed.

Which AI technology is most commonly used for fraud detection?

Machine learning models analyzing behavioral patterns and transaction data in real time are the most widely deployed AI technology for fraud detection in eCommerce.

Can AI fraud detection stop friendly fraud?

AI fraud detection identifies patterns associated with friendly fraud, including repeat false claims, policy abuse, and suspicious dispute timing; however, fully stopping friendly fraud also requires strong evidence collection and automated chargeback management.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.