Credit card fraud is the unauthorized use of someone’s credit card or account information to make purchases, withdraw cash, or open new accounts. Over 60 million Americans experience it each year, and the financial fallout hits both consumers and merchants hard. Learn how credit card fraud works, the most common types you’ll encounter, and who bears the financial losses from this guide.

What Is Credit Card Fraud?

Credit card fraud is the unauthorized use of your credit card or account information to make purchases, withdraw cash, or open new accounts without your permission. It’s a form of identity theft that affects over 60 million Americans each year, and the financial damage extends far beyond consumers—merchants lose billions annually to fraud-related chargebacks and stolen merchandise.

Once someone gets hold of your card details, they can do a lot of damage quickly. They might rack up online purchases, pull cash from ATMs, or even open entirely new credit accounts in your name. The tricky part? You might not notice for weeks.

How Credit Card Fraud Works

Criminals have gotten creative about stealing payment information. Recent research shows just how widespread the problem has become: more than 60 million Americans experienced credit card fraud last year, and notably, only 5% of fraudulent charges involved a physically stolen card, with the vast majority of fraud occurring remotely through data breaches, skimming, and credential theft.

Before criminals can use your card, they first have to get the data through the following common methods.

- Skimming and shimming: Fraudsters attach hidden devices to ATMs, gas pumps, or checkout terminals that copy your card’s magnetic stripe or chip data. The transaction looks completely normal while your information gets stolen in the background.

- Data breaches: Hackers break into retailer or bank databases and steal payment information in bulk. Your card details might sit in a stolen database for months before anyone uses them.

- Phishing and smishing: Fake emails or texts pretending to be from your bank ask you to verify your account or click a suspicious link. The urgency in the message is intentional, designed to make you act before you think.

- Malware: Software installed on your computer or phone records your keystrokes or pulls saved payment data. This often happens through infected downloads or compromised websites.

Understanding these credit card fraud methods matters because the theft itself usually happens long before the fraudulent charge appears on a statement. That gap between when data is stolen and when it’s actually used gives merchants a real opportunity to catch fraud in progress, provided their detection systems know what to look for. This is exactly why eCommerce fraud detection tools focus on behavioral signals and transaction patterns rather than assuming a card number alone proves who’s really making the purchase.

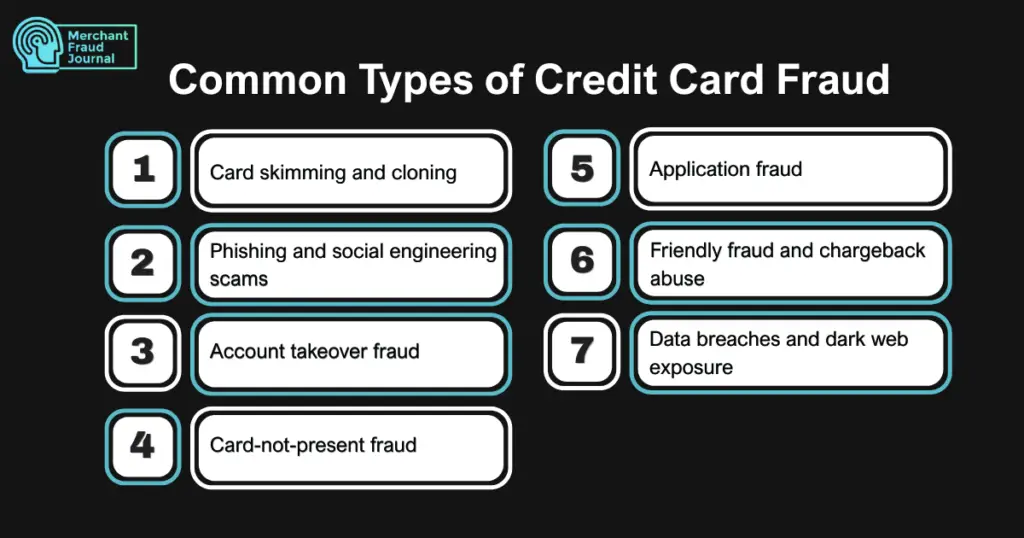

Common Types of Credit Card Fraud

Understanding how credit card fraud operates is essential for spotting it before it drains your revenue. According to Chargeflow, Mastercard now attributes about 70% of all credit card fraud to friendly fraud alone, a shift that has pushed merchants toward absorbing far more in annual losses than third-party card theft ever did. The types below range from old-school card cloning to newer, harder-to-detect schemes that exploit trust rather than technology.

Card skimming and cloning

When criminals capture your card data through a skimming device, they can create a physical clone card that works just like the original. The cloned card looks legitimate and functions normally at checkout, which makes it hard for merchants to catch without chip verification.

Phishing and social engineering scams

Beyond just stealing data, social engineering tricks people into handing over their card details willingly. Fake websites that look identical to your bank’s login page, phone calls from fraud departments, and urgent messages about account closures are all common tactics.

Account takeover fraud

Account takeover happens when someone gains access to your existing credit card account and changes the password, PIN, or contact information. Once they’re in control, they can make purchases, drain funds, and lock you out entirely.

Card-not-present fraud

Card-not-present (CNP) fraud involves using stolen card numbers to buy things online or over the phone, no physical card required. This is the most common type of fraud for eCommerce merchants because there’s no way to examine the card or verify the buyer’s identity in person.

Application fraud

With application fraud, criminals use stolen personal information like your Social Security number to open a brand new credit card in your name. Unlike account takeover, you might not discover this until you check your credit report or start getting collection notices for accounts you never opened.

Friendly fraud and chargeback abuse

Friendly fraud is a different animal. This happens when a real customer makes a legitimate purchase, receives the product, and then disputes the charge anyway, claiming fraud, non-delivery, or some other issue. While it’s technically not criminal fraud in most cases, it costs merchants billions every year and gets processed through the same chargeback system as real fraud.

Data breaches and dark web exposure

Stolen card data from breaches often ends up for sale on dark web marketplaces, where criminals buy it in bulk. This explains why fraud can show up months or even years after a breach, since your information may have changed hands several times before someone actually uses it.

Merchants who understand these patterns can better tailor their defenses, pairing tools like AVS and 3D Secure for card-not-present transactions with dispute management systems built to catch friendly fraud after the sale. To consistently protect your business from credit card fraud, make sure you stay informed about how each type operates is the first step toward protecting both revenue and customer relationships.

Real Examples of Credit Card Fraud

Fraud plays out differently depending on the type, but a few scenarios come up again and again. A cardholder notices several small charges (often under $5) from merchants they don’t recognize. Fraudsters use small test transactions to confirm a card works before making bigger purchases, which often compels victims to shrug and report the credit card fraud.

A merchant ships an order with tracking confirmation, only to receive a chargeback weeks later claiming the item never arrived. The customer received the product but disputed the charge anyway. Someone gets an email saying their password was changed, but they didn’t do it. By the time they regain access to their account, unauthorized purchases have already gone through.

Who Is Liable for Credit Card Fraud Losses

Liability depends on the transaction type and who’s involved. Understanding these rules matters because merchants who don’t know where liability falls often end up absorbing costs that could have been shifted elsewhere through proper authentication or documentation.

| Party | Typical Liability |

|---|---|

| Consumers | Generally capped at $50 under federal law; most issuers offer zero liability |

| Merchants | Bear losses for CNP fraud and chargebacks in most cases |

| Card Issuers | Absorb losses for certain fraud types, especially chip-verified transactions |

The liability shift that came with EMV chip adoption moved more responsibility to merchants for card-present fraud when they don’t support chip transactions. For eCommerce, merchants typically absorb the biggest losses since CNP transactions lack the same verification protections.

How AI and Machine Learning Detect Credit Card Fraud

Modern fraud detection relies on artificial intelligence (AI) and machine learning to spot suspicious patterns in real time. These systems analyze hundreds of data points per transaction (e.g., device fingerprints, IP addresses, behavioral patterns, purchase history), and generate risk scores before orders ship. It is designed to detect and prevent credit card fraud.

Network intelligence takes this further by identifying patterns across thousands of merchants. A fraudster who successfully exploits one store can be flagged across the entire network, protecting other merchants from the same bad actor. The most effective systems adapt continuously, learning from new fraud patterns without manual intervention.

Stop Credit Card Fraud Before It Ruins Your Business

Credit card fraud rarely announces itself before it hits. The businesses that survive and grow are the ones that treat fraud prevention as a continuous priority rather than a reaction to a bad month, layering pre-transaction screening with strong post-purchase dispute management. Taking action now, before fraud losses pile up, protects not just your revenue but your ability to keep accepting card payments at all.

Frequently Asked Questions

What qualifies as credit card fraud?

Any unauthorized use of a credit card or card information to make purchases, withdraw funds, or open accounts without the cardholder's permission qualifies as credit card fraud. This includes both third-party fraud (stolen cards) and first-party fraud (friendly fraud committed by the cardholder).

How is credit card fraud proven?

Fraud is typically proven through transaction records, IP addresses, device fingerprints, shipping addresses that don't match the cardholder, and lack of authentication like CVV or 3D Secure verification. For merchants fighting chargebacks, compelling evidence includes delivery confirmation, customer communication logs, and proof of prior transactions.

Do police investigate credit card fraud cases?

Local police often take reports for documentation, but most credit card fraud cases are handled by federal agencies like the FTC or FBI, especially when they involve large-scale or cross-border criminal activity. Individual cases under a few thousand dollars rarely receive dedicated investigation resources.

Can merchants recover money lost to credit card fraud?

Merchants can recover losses by fighting chargebacks with compelling evidence, though win rates vary by reason code and evidence quality. Prevention and automated dispute management typically deliver better results than trying to recover funds after the fact.

How long does it take to resolve a credit card fraud case?

Resolution time varies, but many issuers can reverse fraudulent charges within a few business days to a couple of weeks. More complex cases, such as identity theft involving new accounts, may take longer and require additional documentation.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.