Navigating the world of high-risk merchant accounts can be a daunting task, especially when it comes to securing approval for payment processing. Businesses operating in high-risk industries often face unique challenges, including account shutdowns and payment processing delays.

This article aims to demystify the process of obtaining a merchant account. It also touches on the concept of instant approval when you apply for a high-risk merchant account, and provide actionable insights for business owners.

What Is a High-Risk Merchant Account?

A high-risk merchant account is a specialized payment processing solution designed for businesses that operate in industries deemed high-risk by financial institutions. These industries often include sectors such as travel, adult entertainment, CBD products, nutraceuticals, and subscription services. The classification as high-risk typically arises from factors such as high chargeback rates, regulatory scrutiny, and the potential for fraud.

Understanding Pre-Approval vs. Approval

For high-risk merchants, the path to securing a merchant account involves two distinct stages that are often confused. Knowing the difference between pre-approval and final approval helps set realistic expectations and prepares businesses for what lies ahead. Each stage serves a specific purpose in the payment processor’s evaluation process.

- Pre-approval: This is a preliminary assessment that indicates a potential fit for a merchant account. It does not guarantee final approval and often requires further documentation and review.

- Final Approval: This is the stage where the payment processor conducts a comprehensive evaluation of the business, including risk analysis and compliance checks.

Receiving pre-approval is an encouraging sign, but merchants should continue preparing thorough documentation to support the final review. A clear understanding of both stages allows businesses to engage with payment processors more confidently and avoid unnecessary delays.

What Is the Approval Process for High-Risk Merchant Accounts?

Obtaining a high-risk merchant account involves several key steps. Each designed to assess the viability and risk associated with the business. Understanding this process can help streamline your application and improve your chances of approval.

Step 1: Application submission

The journey begins with submitting an application that includes essential business details. It is vital to ensure that the application is complete and accurate to avoid delays. Processors typically request information, such as business registration documents, processing history, and ownership details.

Step 2: Underwriting review

Once the application is submitted, it enters the underwriting phase. Underwriters will evaluate various factors, including:

- Business model: Understanding how the business operates and its revenue generation methods.

- Chargeback history: Analyzing past chargeback rates to assess risk.

- Financial stability: Reviewing financial documents to ensure the business can handle potential disputes.

This phase can take anywhere from a few days to several weeks. This will depend on the complexity of the business and the completeness of the submitted documentation. Merchants with elevated chargeback histories or unconventional revenue models should expect more detailed scrutiny during this stage.

Step 3: Risk assessment

Following the underwriting review, a risk assessment is conducted. This involves evaluating the potential for fraud (e.g., eCommerce fraud) and compliance with regulations, such as Know Your Customer (KYC) and Anti-Money Laundering (AML) laws.

Processors may also examine the business’s geographic exposure, the nature of its customer base, and its existing high-risk merchant fraud prevention measures. Demonstrating a proactive approach to compliance and risk management can strengthen the application at this stage.

Step 4: Final approval

After completing the risk assessment, the underwriters will make a decision regarding the application. If approved, the merchant account will be set up, and the business can begin processing payments.

Some processors may impose conditions on approval. These conditions may include rolling reserve or transaction volume caps, particularly for businesses deemed higher risk. Reviewing these terms carefully before signing ensures there are no surprises once processing begins.

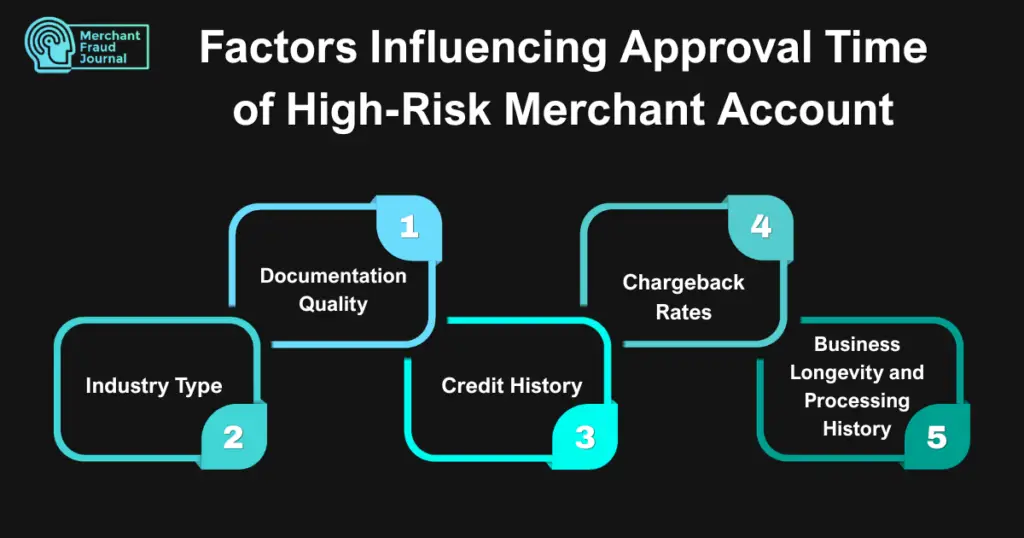

5 Factors Influencing Approval Time of High-Risk Merchant Account

Several factors can impact the time it takes to secure a high-risk merchant account. Understanding these elements can help businesses prepare effectively. The stakes are considerable given that first-party fraud now represents a third of all reported fraud globally, accounting for a $132 billion risk to eCommerce in 2024 alone. That said, here are the factors to look into when seeking instant or accelerated approval time for high-risk merchant accounts:

1. Industry type

Certain industries are inherently riskier than others. For example, businesses in the gambling or adult entertainment sectors may face stricter scrutiny compared to those in retail.

Processors classify industries based on historical fraud rates, regulatory complexity, and chargeback exposure, all of which directly shape how deeply an application is reviewed. Merchants operating in heavily regulated verticals should anticipate a longer underwriting timeline. They should also prepare for more detailed questions about their compliance practices.

2. Documentation quality

Providing complete and accurate documentation can significantly expedite the approval process. Essential documents may include:

- Business registration and licensing documents

- Recent bank statements

- Processing history from previous providers

- Government-issued ID for the business owner

Incomplete or inconsistent documentation is one of the most common reasons approvals are delayed, as underwriters must pause the review to request missing information. Ensuring that all submitted materials are current, legible, and consistent with the details provided in the application removes a major source of friction from the process.

3. Credit history

A strong credit history can positively influence the approval process. Conversely, a poor credit score may lead to additional scrutiny or even denial.

Processors view credit history as an indicator of financial responsibility. It also determines the likelihood that a merchant can absorb potential losses from disputes or refunds. Merchants with blemished credit histories can improve their standing by addressing outstanding debts and providing a written explanation of any past financial difficulties alongside their application.

4. Chargeback rates

High chargeback rates can raise red flags for underwriters. Businesses should implement chargeback prevention strategies to maintain a favorable risk profile.

Most processors consider a chargeback ratio above 1% a threshold for concern. Rates significantly above that level can result in outright denial or the imposition of a rolling reserve. Proactively sharing a chargeback mitigation plan with the processor demonstrates awareness of the issue and a commitment to keeping dispute rates in check.

5. Business longevity and processing history

The length of time a business has been operating is a meaningful signal of stability for underwriters evaluating high-risk applications. A merchant with several years of consistent processing history presents far less uncertainty than a newly launched business with no track record to assess.

Processors are more likely to expedite approvals for established merchants who can demonstrate steady transaction volumes and a history of low dispute rates. Startups or recently restructured businesses entering high-risk categories should expect a more cautious review and may benefit from starting with a smaller processing limit to build credibility over time.

The Myth of Instant Approval

Many businesses are drawn to advertisements promising high-risk merchant account instant approval. However, it is crucial to understand that true instant approval is largely a myth. While some providers may offer rapid pre-approval, the actual approval process typically takes longer due to the inherent risks involved.

Merchant account approval standards have grown stricter in recent years, with high chargeback ratios, fraud exposure, and industry type all facing heavier scrutiny than before. Some providers now ask merchants to demonstrate how they will handle disputes before an account is even opened. This reflects a shift where chargebacks are no longer just a performance metric but a central factor in whether approval is granted.

The scale of risk that underwriters must account for helps explain why shortcuts are rarely possible. Consumers disputed up to $105 million charges with U.S. card issuers in 2024, worth an estimated $11 billion, up from $7.2 billion in 2019. On the other hand, friendly fraud cases are forecast to rise 40% by 2026. With exposure at this level, processors have a strong incentive to conduct thorough due diligence before approving any high-risk account, regardless of how quickly a merchant needs to begin processing.

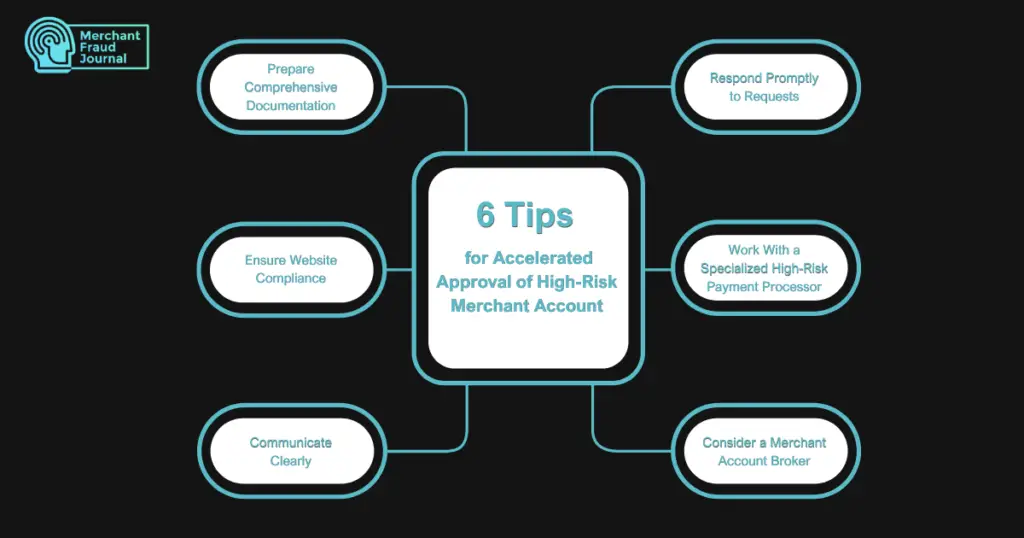

6 Tips for Accelerated Approval of High-Risk Merchant Account

While instant approval may not be feasible, there are several strategies businesses can employ to expedite the approval process for high-risk merchant accounts.

1. Prepare comprehensive documentation

Documentation remains as the foundation of any successful high-risk merchant account application, and gaps in paperwork are one of the most common reasons reviews are delayed. Having all necessary documents ready before applying can save time.

Processors evaluating high-risk applications also often request supplementary materials such as processing statements from the past three to six months, voided business checks, and chargeback ratio reports. Organizing these documents into a single, clearly labeled submission package signals professionalism and reduces the likelihood of follow-up requests that stall the review.

2. Ensure website compliance

A compliant website is crucial for approval. Before submitting your application, conduct a thorough audit of your site to confirm it meets the standards most processors expect from high-risk merchants. Ensure that your site includes:

- Clear product descriptions

- Transparent pricing

- Refund and return policies

Underwriters routinely visit merchant websites as part of the review process, and a site that appears incomplete or inconsistent with the application details can trigger additional scrutiny. Verifying that all pages are live, functional, and accurately reflect the business before submitting the application removes a common source of delays.

3. Communicate clearly

Underwriters are trained to spot inconsistencies, and even minor discrepancies between what an application states and what a business actually does can trigger delays or outright rejection. When filling out the application, be transparent about your business model and operations. Clearly explain:

- What products or services you offer

- Your target audience

- Your marketing strategies

Processors are more cautious about applications that appear vague or leave room for misinterpretation, particularly for businesses in industries with a history of compliance issues. Providing a brief written overview of the business alongside the application can add helpful context that the standard form fields may not capture.

4. Respond promptly to requests

Underwriters may request additional information during the review process. Responding quickly to these requests can help keep the process moving smoothly. Delays in responding are one of the most avoidable reasons applications stall, as processors often work through multiple reviews simultaneously and may deprioritize applications awaiting a response.

Designating a single point of contact within the business who is responsible for handling underwriter communications ensures that no request goes unaddressed for longer than necessary.

5. Work with a specialized high-risk payment processor

Not all payment processors are equipped to handle high-risk accounts, and applying to the wrong ones wastes time. For example, a CBD merchant applying to a general-purpose processor will likely face rejection, while applying for a high-risk merchant account at (High Risk Pay) highriskpay.com, a processor that specializes in high-risk industries. This is because the underwriting team is already familiar with the compliance requirements and risk profile typical of that business type.

Seeking out processors that specialize in high-risk industries increases the likelihood of a smoother, faster review since their underwriting teams are already familiar with the risks and compliance requirements associated with your business type.

6. Consider a merchant account broker

A broker with established relationships in the high-risk payments space can match your business with processors most likely to approve your application. Rather than submitting multiple individual applications and waiting on each outcome, a broker streamlines the process and can often advocate on your behalf during underwriting, reducing the overall time to approval.

Taking the Right Steps Toward High-Risk Merchant Account Approval

Securing a high-risk merchant account can be a complex process, but understanding the nuances of approval can significantly enhance your chances of success. While instant approval may not be a reality, thorough preparation and a clear understanding of the approval process can lead to a smoother experience.

Frequently Asked Questions

How long does the underwriting process usually take?

While low-risk accounts might take a day or two, a proper high-risk underwriting process usually takes between 2 to 7 business days. This timeline depends heavily on the complexity of your business model and how quickly you provide requested documents.

What are the typical fees associated with a high-risk merchant account?

High-risk merchants generally pay higher processing rates, typically ranging from 2.5% to 5% per transaction. You may also encounter additional setup fees, monthly maintenance fees, or higher chargeback penalties compared to standard accounts.

What is a rolling reserve, and will I need one?

A rolling reserve is a standard risk-mitigation tool where the processor holds a percentage of your daily revenue (usually 10% to 20%) for a set period, like 180 days. This money acts as a protective buffer to cover potential future chargebacks or fraud spikes.

What website compliance mistakes can cause my application to be denied?

Failing to clearly state your refund, privacy, and shipping policies on your website is a major red flag for underwriters. Applications are also frequently rejected if product descriptions are vague or if the pricing structure appears misleading to consumers.

How do I maintain a good relationship with my processor after approval?

You should monitor your chargeback ratio weekly and utilize fraud prevention alerts to resolve disputes before they escalate. It is also important to maintain consistent transaction patterns and proactively notify your processor of any major shifts in your business model or sales volume.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.