High-risk merchants lose more revenue to fraud and chargebacks than any other merchant category; and the gap is widening. Fraudsters specifically target businesses they know have higher approval thresholds and fewer resources to fight back.

The classification itself creates a vicious cycle. Elevated fraud rates lead to higher processing fees and stricter monitoring, which strains operations and leaves less budget for prevention. This guide breaks down why high-risk merchants face disproportionate fraud exposure, the specific threats you’re up against, and the layered defenses that actually work to protect revenue and keep your merchant account intact.

High-Risk Merchant Explained

A high-risk merchant is any business that payment processors and card networks have classified as posing a greater-than-average financial or reputational risk. This classification isn’t arbitrary, and it stems from a structured assessment of several key business characteristics that signal elevated exposure to fraud, chargebacks, or regulatory scrutiny.

The impact of this classification on the global economy is substantial and growing rapidly. The global high-risk payments market is set to be at $16.4 billion by 2034 in terms of reach and is projected to expand significantly as digital commerce evolves.

Evaluating high-risk merchants

| Evaluation Factor | Risk Description & Impact |

|---|---|

| Chargeback History | Chargebacks, which are transactions disputed and reversed by cardholders, are among the most telling indicators. A merchant whose chargeback ratio consistently exceeds 1% of monthly transactions raises immediate red flags. Even a single spike can trigger a review, and a pattern of disputes signals poor fraud controls, customer dissatisfaction, or both. |

| Industry Type | Certain industries carry inherent risk regardless of how well-run a business is. Adult content, online gambling, travel, nutraceuticals, firearms, cryptocurrency exchanges, and subscription-based services are routinely flagged because of their historically high dispute rates, complex regulatory environments, or association with fraudulent activity across the sector. |

| Business Model | How a merchant sells matters just as much as what they sell. Businesses with recurring billing cycles, high average transaction values, card-not-present sales, or long fulfillment windows between payment and delivery create more opportunities for disputes and fraud to emerge, making the payment processor's exposure harder to predict and control. |

| Processing History | New businesses without an established payment history present an unknown risk profile by default. Merchants who have previously lost a processing account, been placed on the MATCH list (a blacklist maintained by Mastercard for terminated merchants), or who have a thin or inconsistent transaction record face tighter scrutiny during underwriting. |

Being labeled high-risk doesn’t mean a business is fraudulent or poorly managed. It means the processor has calculated that working with that business carries a higher potential cost. As a result, high-risk merchant accounts typically face higher processing fees, rolling reserves (where a percentage of revenue is held back as a financial buffer), stricter contract terms, and in some cases, limited access to mainstream payment processors altogether.

Why High-Risk Merchants Are More Vulnerable to Fraud

High-risk status increases fraud exposure through several interconnected factors. Higher transaction volumes mean more opportunities for fraudsters to hide among legitimate orders. Card-not-present environments make confirming cardholder identity significantly harder without physical card verification.

Fraudsters also know high-risk merchants may have less sophisticated defenses or be more desperate for sales. In fact, while the average e-commerce business loses about 3% of its revenue to fraud, that figure often climbs to 5% or higher in high-risk markets according to data from Mastercard.

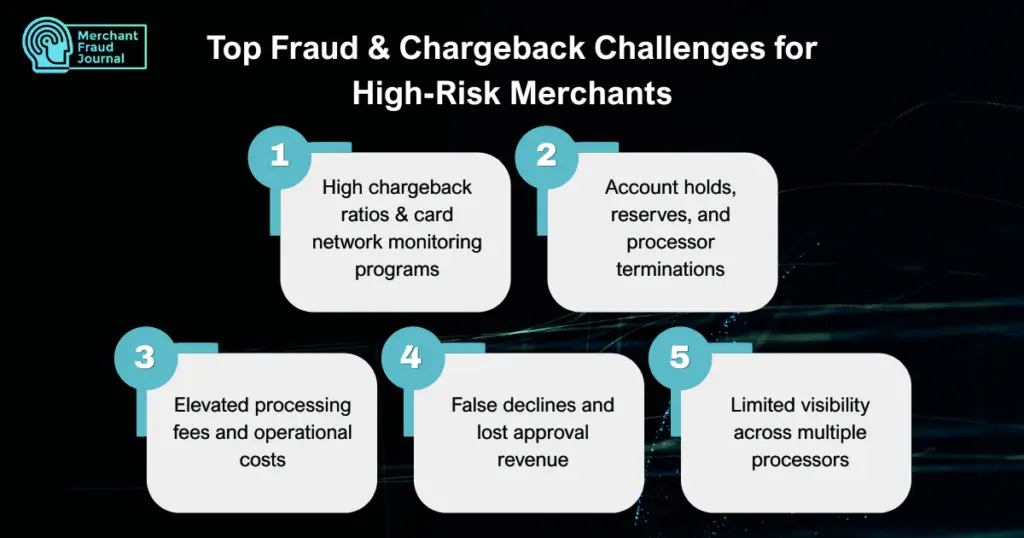

Top Fraud and Chargeback Challenges for High-Risk Merchants

Even one of the following issues can destabilize your payment processing. Multiple challenges create serious operational strain. The fragility of the payment pipeline is heavily reflected in modern commercial data. According to The Baymard Institute’s 2026 UX Meta-Analysis, the global average cart abandonment rate sits at 70.22%, heavily driven by complex checkout flows, hidden fees, and lacking payment options.

Here are the key challenges high-risk merchants face regarding eCommerce fraud and chargebacks.

1. High chargeback ratios and card network monitoring programs

Your chargeback ratio (chargebacks divided by total transactions) determines whether you enter costly monitoring programs. Visa’s VAMP and Mastercard’s ECM programs impose significant fees and operational requirements on merchants who exceed thresholds. Once you’re in a monitoring program, getting out takes months of sustained improvement.

2. Account holds, reserves, and processor terminations

When ratios exceed thresholds, processors respond with rolling reserves (holding a percentage of your revenue), fund holds, and potential MATCH/TMF listing. Being placed on the MATCH list effectively blacklists you from most payment processors.

3. Elevated processing fees and operational costs

High-risk merchants pay premium processing rates, often 1-2% higher than standard merchants, plus additional per-chargeback fees. These compounding costs can significantly erode profit margins, making it essential for high-risk businesses to factor payment processing expenses into their pricing strategy from the outset.

4. False declines and lost approval revenue

Overly aggressive fraud rules block legitimate customers and cost revenue. Finding the right balance between protection and approval rates is an ongoing challenge. Every declined transaction from a genuine customer not only means immediate lost revenue. It can also permanently damage brand loyalty, as frustrated shoppers often turn to competitors who offer a smoother checkout experience.

5. Limited visibility across multiple processors

Multi-processor setups create blind spots for tracking disputes and fraud patterns. When your data lives in silos, you can’t see the full picture of what’s happening across your business. This fragmented view makes it nearly impossible to identify recurring issues, spot coordinated fraud, or make informed decisions about where to optimize your payment stack.

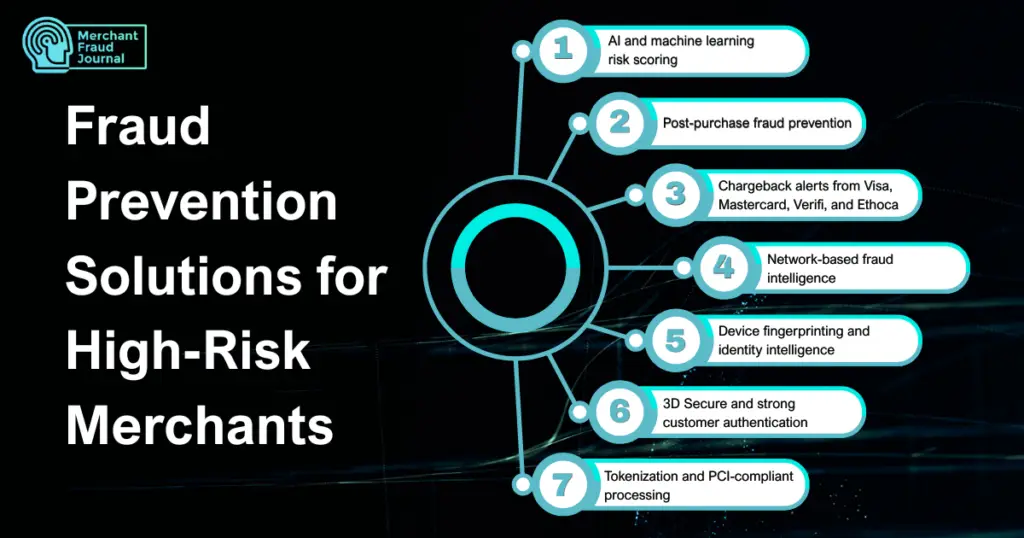

Fraud Prevention Solutions for High-Risk merchants

No single solution stops the various types of eCommerce fraud; you want defense in depth. High-risk merchants face an increasingly aggressive and automated threat landscape. Relying on a single firewall or standard CVV check leaves massive blind spots.

To protect your margins, you need a multi-layered security posture that addresses both automated cyberattacks and malicious consumer behavior that may include the following.

1. AI and machine learning risk scoring

Real-time transaction scoring adapts to evolving fraud patterns without static rules. Unlike rule-based systems that fraudsters quickly learn to circumvent, ML models continuously learn from new data. Research shows that 90% of surveyed financial professionals reported a distinct increase in AI-driven attacks, underscoring the necessity for models that continuously self-correct in real time rather than waiting for manual rule updates.

2. Post-purchase fraud prevention

Post-checkout fraud detection analyzes orders after authorization but before fulfillment. This approach avoids checkout friction while still catching suspicious orders before you ship. Some platforms analyze transactions against networks of thousands of merchants to identify known bad actors. Advanced machine learning models cross-reference these network insights with device fingerprinting and behavioral data to spot hidden anomalies in real time.

3. Chargeback alerts from Visa, Mastercard, Verifi, and Ethoca

Chargeback alerts intercept disputes before they become chargebacks. When a cardholder initiates a dispute, you receive an alert and can issue a rapid refund, deflecting the chargeback entirely and avoiding the associated fees. It resolves customer grievances in real time while maintaining a clean merchant processing history.

4. Network-based fraud intelligence

Shared merchant networks flag known bad actors across multiple businesses. When a fraudster hits one merchant, that information protects thousands of others. It creates an immediate defensive shield, shutting down the attacker’s tactics before they can impact the rest of the network.

5. Device fingerprinting and identity intelligence

Device fingerprinting links device, IP, email, and behavioral signals to identify repeat fraudsters. Even when fraudsters use new payment credentials, their device characteristics often give them away. This persistent tracking allows security systems to flag suspicious behavior in real time, stopping bad actors before a transaction can even be completed.

6. 3D Secure and strong customer authentication

3D Secure (3DS) and Strong Customer Authentication (SCA) require multi-factor authentication for transactions. The liability shift benefit means the issuing bank (not you) bears responsibility for fraudulent chargebacks on authenticated transactions. However, the additional friction can reduce conversion rates.

7. Tokenization and PCI-compliant processing

Tokenization replaces sensitive payment data with non-sensitive tokens, protecting stored payment information from breaches. According to data from Visa, token-based transactions drive an average 30% reduction in online fraud compared to traditional PAN (Permanent Account Number) transactions, while simultaneously providing a 4% uplift in transaction authorization rates.

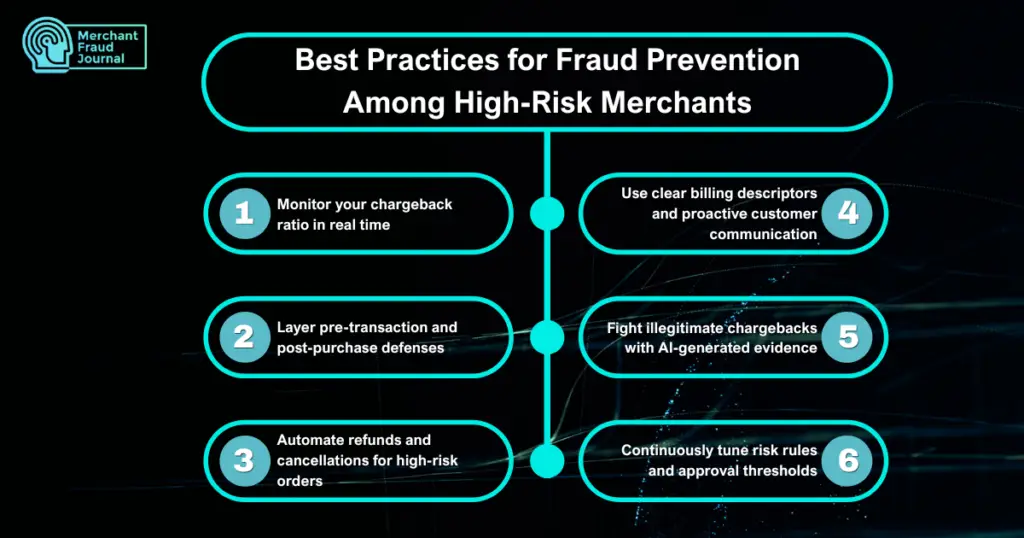

Best Practices for Fraud Prevention and Chargeback Management Among High-Risk Merchants

Layer the following best practices to build comprehensive merchant fraud protection. Combining the following distinct security measures ensures that a vulnerability in one area won’t leave your entire system exposed.

1. Monitor your chargeback ratio in real time

Proactive tracking before thresholds are breached gives you time to respond. Unified dashboards that consolidate data across multiple processors eliminate blind spots and provide early warning when ratios trend upward. Catching these spikes early allows you to pause problematic marketing campaigns or address fulfillment issues before your merchant account is penalized.

2. Layer pre-transaction and post-purchase defenses

Defense-in-depth means combining pre-authorization fraud checks with post-purchase verification for orders that pass initial screening. Implementing this multi-layered approach ensures that high-risk behavior is caught at the storefront while subtle, post-checkout anomalies are flagged before fulfillment.

3. Automate refunds and cancellations for high-risk orders

Automated workflows based on risk scores reduce manual review burden and stop fraud faster. Setting up immediate triggers ensures that flagged transactions are neutralized before fulfillment even begins. With this eCommerce fraud prevention best practice, merchants can instantly reverse suspicious charges to completely eliminate the threat of costly chargebacks.

4. Use clear billing descriptors and proactive customer communication

Unclear statements cause “I don’t recognize this” chargebacks, one of the most preventable dispute types. Order confirmations, shipping notifications, and recognizable billing descriptors remind customers what they purchased. Providing a direct link to a 24/7 customer support chat within those digital receipts allows buyers to quickly resolve confusion before contacting their bank.

5. Fight illegitimate chargebacks with AI-generated evidence

The representment process lets you challenge invalid chargebacks with evidence. Automated evidence collection and submission improves win rates while reducing the manual work of building dispute responses. Deploying machine learning models to instantly cross-reference transaction history, delivery receipts, and user behavior ensures that your dispute packages are both highly persuasive and completely optimized for card network rules.

6. Continuously tune risk rules and approval thresholds

Ongoing optimization means analyzing declined transactions, adjusting scoring models, and balancing fraud prevention with approval rates. What worked last quarter may not work today. Fraudsters adapt, and your defenses adapt with them. Regularly scheduling these audits ensures that genuine customers experience seamless checkouts while malicious actors are blocked in real-time.

Ensuring Long-Term Success for High-Risk Businesses

As you continue to navigate the complexities of high-risk merchandising, remember that staying informed and proactive is key. Emphasizing the importance of a high-risk merchant account, utilizing advanced fraud detection tools, and building a strong compliance framework are crucial steps in your fraud prevention journey. Educating your team and prioritizing customer verification further strengthens your defense against fraud, allowing you to operate with confidence and security.

Frequently Asked Questions

What chargeback ratio triggers a card network monitoring program?

Visa's VAMP and Mastercard's ECM programs activate when dispute ratios exceed network-defined thresholds, typically calculated as chargebacks divided by total transactions over a rolling period.

Can a high-risk merchant ever be reclassified as low-risk?

Yes, merchants who maintain low chargeback ratios, demonstrate stable processing history, and implement strong fraud prevention may qualify for reclassification over time.

Are pre-transaction fraud tools enough for high-risk businesses?

No, pre-transaction tools alone miss friendly fraud and policy abuse that occur after authorization. High-risk merchants benefit from layering post-purchase prevention and chargeback alerts for comprehensive protection.

How quickly can chargeback alerts start preventing disputes?

Most chargeback alert services activate within one to two business days and begin intercepting disputes in real time as soon as the integration is live.

What is the difference between friendly fraud and third-party fraud?

Friendly fraud occurs when a legitimate cardholder disputes their own valid purchase, while third-party fraud involves unauthorized use of stolen payment credentials by someone other than the cardholder.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.