A stolen card number now travels faster than the fraud alert meant to stop it. Criminals test compromised credentials in seconds, route stolen funds through cryptocurrency within minutes, and disappear before a chargeback ever lands on a merchant’s desk. For fraud prevention teams, risk analysts, and eCommerce operators, the numbers behind that speed tell the real story of where the threat stands.

Here are the latest credit card statistics merchants must know in 2026, along with their potential implications and what you must do next.

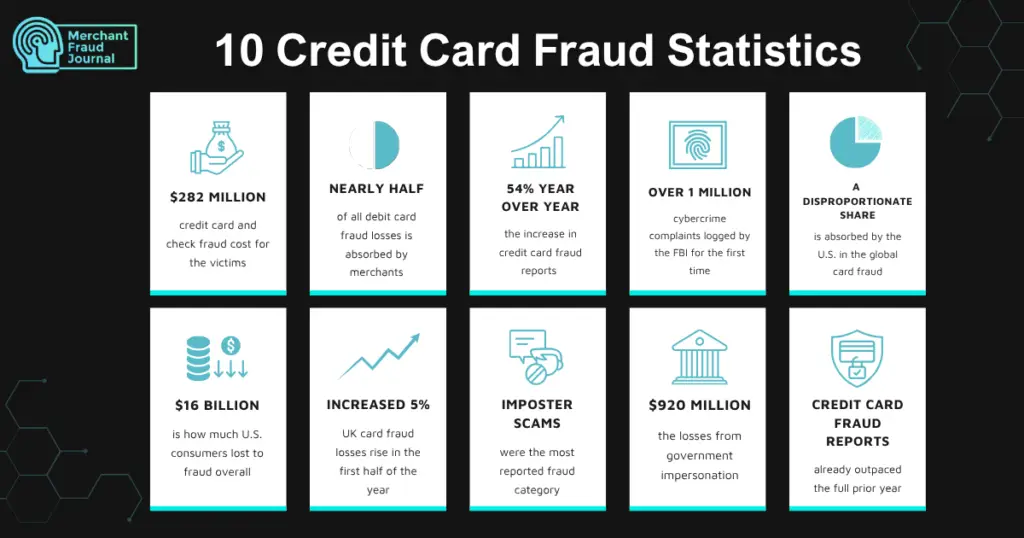

1. Credit Card and Check Fraud Cost Victims $282 Million

Within that broader total, credit card and check fraud specifically accounted for $282 million in reported losses, per IC3 data. The figure sits well below losses from investment scams or business email compromise, a reminder that card fraud, while high in volume, tends to produce smaller individual losses than other cyber-enabled crimes.

Credit card fraud chips away at margins through thousands of small chargebacks, each one carrying its own dispute fee and processor penalty. Tracking a monthly chargeback ratio against network thresholds, rather than watching for a single large loss, gives a more accurate picture of exposure and helps merchants catch a drifting trend before it triggers a high-risk designation.

2. Merchants Now Absorb Nearly Half of All Debit Card Fraud Losses

Merchants paid for 49.9% of debit card fraud losses in 2023, up from 46.9% in 2021, while the share paid by banks dropped from 33.4% to 28.3% over the same period, according to the Federal Reserve’s biennial report on debit card transactions.

That shift in liability means issuer-side protections can no longer be treated as a merchant’s primary line of defense. Relying on the bank to catch fraud after the fact is a losing strategy when merchants are the ones increasingly left holding the loss.

Invest directly in AVS (address verification service) matching, 3D Secure authentication, and velocity checks at checkout. Do not hold back in negotiating dispute terms into processor contracts, and have more control over a cost that keeps sliding in their direction.

3. Credit Card Fraud Reports Jumped 54% Year Over Year

Momentum accelerated further in 2025. Credit card fraud reports climbed sharply through the first three quarters of the year compared with the same period in 2024, continuing a multi-year trend that the Federal Trade Commission’s (FTC) own Consumer Sentinel exploration tools track on a rolling quarterly basis.

A jump of that size usually points to more stolen card data circulating and being tested against live checkout flows, a pattern known as carding. Merchants who see a spike in small-value authorizations, especially from new accounts or unusual IP ranges, are often watching this exact trend play out in real time. Rate limiting on payment endpoints and flagging rapid small-dollar authorization attempts can catch card testing before it escalates into larger fraudulent purchases.

4. The FBI Logged Over 1 Million Cybercrime Complaints for the First Time

Total complaints filed with the FBI’s Internet Crime Complaint Center surpassed 1 million for the first time in the center’s history, reaching 1,008,597 complaints with reported losses of $20.877 billion, a 26% jump, according to the FBI’s IC3 Annual Report.

Milestones like this one signal that fraud detection models built on prior years’ patterns are aging out faster than usual. Merchants operating with static, rules-based fraud filters are effectively fighting last year’s threat with this year’s attack volume.

Take time to review fraud rules on a quarterly rather than annual cycle, and pool anomaly data with industry peers or a shared fraud consortium. Doing so helps merchants keep pace with a threat landscape that is scaling faster than most internal review cycles.

5. The U.S. Absorbs a Disproportionate Share of Global Card Fraud

American merchants and issuers carry far more than their fair share of the burden. Cards issued in the United States accounted for 25.29% of total card volume worldwide in 2023 but 42.32% of worldwide fraud losses, according to Nilson Report data.

That imbalance matters for any merchant selling to American cardholders, regardless of where the business itself is based. Treating U.S. transactions as inherently lower risk because of market size or familiarity is a costly assumption. Applying the same rigorous verification tooling, address matching, and device fingerprinting to domestic U.S. orders that a merchant might reserve for cross-border transactions helps close the gap.

6. U.S. Consumers Reported Losing $16 Billion to Fraud Overall

Total fraud losses reported to the Federal Trade Commission reached roughly $16 billion, the highest figure on record and an increase of about 25%, according to the FTC. Much of that broader fraud total feeds directly into card fraud downstream. This is since personal data harvested through scams and breaches routinely ends up tested against merchant checkout pages months or years later.

Merchants should assume that compromised identity data is more available to attackers than ever before, which makes static identity checks, like matching a name to a billing address, increasingly unreliable on their own. Layering in behavioral signals and device intelligence alongside traditional identity verification gives merchants a better chance of catching fraud built on stolen but technically accurate personal information.

7. UK Card Fraud Losses Climbed 5% in the First Half of the Year

Fraud losses on UK-issued credit, debit, and charge cards totaled £298.9 million in the first six months of the year, a 5% increase over the same period a year earlier, according to UK Finance’s Half Year Fraud Report. Card fraud now represents 6.9 pence of every £100 in card spending.

Losses growing faster than overall card spending is the detail merchants should pay closest attention to. This means fraud is outpacing legitimate transaction volume rather than simply scaling alongside it. UK and EU merchants tracking only their absolute chargeback count can miss this shift entirely. Watching the fraud-to-sales ratio quarter over quarter, rather than the raw loss figure, gives a clearer signal of whether fraud exposure is actually worsening relative to the business’s own growth.

8. Imposter Scams Were the Most Reported Fraud Category

Nearly one in three fraud reports filed with the FTC involved someone pretending to be a bank, a government agency, or another trusted entity. Reported losses to imposter scams reached $3.5 billion, the FTC found, nearly triple what was reported five years earlier.

Merchants selling gift cards, high-value electronics, or anything easily resold are common landing points for these funds. Training checkout and customer service teams to recognize the signs of a victim acting under pressure, such as urgency, unfamiliarity with the product, or a coached explanation for an unusual purchase, can stop laundering activity before it completes.

9. Government Impersonation Losses Topped $920 Million

Within the imposter scam category, people reported losing about $920 million specifically to scammers posing as government officials, per the FTC’s release. Fake security alerts, often impersonating a bank, remain one of the costliest entry points criminals use to convince victims to move money.

Merchants operating anywhere near government-adjacent services, such as tax preparation, licensing, benefits processing, or bill pay, should expect to see fraudulent claims and spoofed correspondence built around this exact playbook. The same social engineering tactics that convince a consumer to wire money to a fake government agency are often redirected toward tricking merchant support staff into refunding, reshipping, or expediting orders.

Build the verification steps into high-risk support requests, particularly ones involving urgency or threats of legal consequence. Doing so closes a door that scammers are actively testing.

10. Credit Card Fraud Reports Already Outpaced the Full Prior Year

Reported cases of credit card fraud reached 503,450 in the first three quarters alone, a figure that already exceeded the total number of reports filed across the entire previous year, based on quarterly FTC Consumer Sentinel Network data. It remains the single largest identity theft category the agency tracks. Growth at that pace means merchants working from an annual fraud review cycle are planning against outdated numbers before the year is even over.

A fraud strategy calibrated last January is already behind the curve by the third quarter. Shifting toward adaptive, machine-learning-based fraud scoring, paired with quarterly strategy reviews instead of annual ones, gives merchants a better chance of tracking a threat that is growing faster than most planning cycles account for.

What the Data Signals for 2026

Card fraud is not slowing down, but it is changing shape. Losses are shifting from card-present to card-not-present channels, from issuers to merchants, and from opportunistic theft to more organized, AI-assisted schemes. Fraud prevention strategies built around chip technology and static rules alone will not keep pace with a threat that has already moved past them.

Frequently Asked Questions

How does credit card fraud compare to other forms of identity theft?

Credit card fraud has been the most common type of identity theft in the United States. It's considered one of the fastest-growing categories of identity theft overall, reflecting how easily stolen card data can be monetized.

Is credit card fraud usually a misdemeanor or a felony?

It depends entirely on the state and the amount involved. Credit card fraud can be either a misdemeanor or a felony depending on the severity of the act and the state where it occurs — for example, it's automatically a felony in Texas, but Florida treats smaller first and second offenses as misdemeanors.

Is credit card fraud the most common form of identity theft?

Yes, in most recent years. For four of the past five years, credit card fraud has been the most common type of identity theft in the United States.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.