False declines occur when legitimate transactions are mistakenly flagged as fraudulent, leading to lost sales and diminished customer trust. These false positives often lurk in the shadows. Unlike chargebacks which merchants can see and react to emotionally as theft, eCommerce false declines pass silently under the radar by definition. In fact, they are even celebrated.

No merchant declines an order they believe to be legitimate; and so every false positive is (incorrectly) feted as a fraudster thwarted. Too many merchants do not understand the true scope of the problem, and so falsely believe these self-inflicted wounds are no big deal. This article discusses how to reduce eCommerce false declines, and the impact of failing to do so.

What Are eCommerce False Declines?

False declines, often referred to as false positives, happen when a valid transaction is rejected by a payment processor or fraud detection system. This rejection can stem from various factors, including overly stringent fraud detection algorithms, technical errors, or discrepancies in customer information.

Beyond the immediate frustration for shoppers, the financial impact is massive. Global eCommerce losses driven by false declines are projected to reach approximately $231 billion, according to data from Datos Insights.

The mechanics behind false declines

When a customer attempts to make a purchase online, their transaction passes through multiple layers of security. These include:

- Payment gateways: These systems validate card details and check for available funds.

- Fraud filters: These algorithms analyze transaction patterns to identify potential eCommerce fraud.

- Bank authorization: The issuing bank also assesses the transaction for legitimacy.

If any of these systems flag the transaction as suspicious, it may be declined, even if the customer is genuine. This process can lead to frustration for both the customer and the merchant.

Common causes of false declines

Several factors contribute to the occurrence of false declines, ranging from outdated legacy fraud systems to rapidly changing consumer behaviors. Often referred to as customer insults, these incorrect rejections occur when legitimate transactions are flagged as fraudulent, leading to immediate revenue loss and severe damage to customer retention.

Knowing why these errors happen is the first step toward reclaiming this lost revenue. The primary drivers include:

- Unusual spending patterns: Transactions that deviate from a customer’s typical spending behavior may be flagged.

- Technical glitches: Errors in the payment processing system can lead to legitimate transactions being declined.

- Inconsistent information: Mismatches between the billing address and the shipping address can trigger a decline.

- High-risk locations: Transactions originating from regions known for fraud may be automatically flagged.

The scale of this issue is immense. eCommerce false declines cost retailers a staggering $443 billion per year globally—an amount that represents nine times more than the cost of actual, successful fraud. Furthermore, roughly 47% of merchants report that these false declines directly eat into their sales, with many estimating that up to 5% of their legitimate orders are incorrectly blocked.

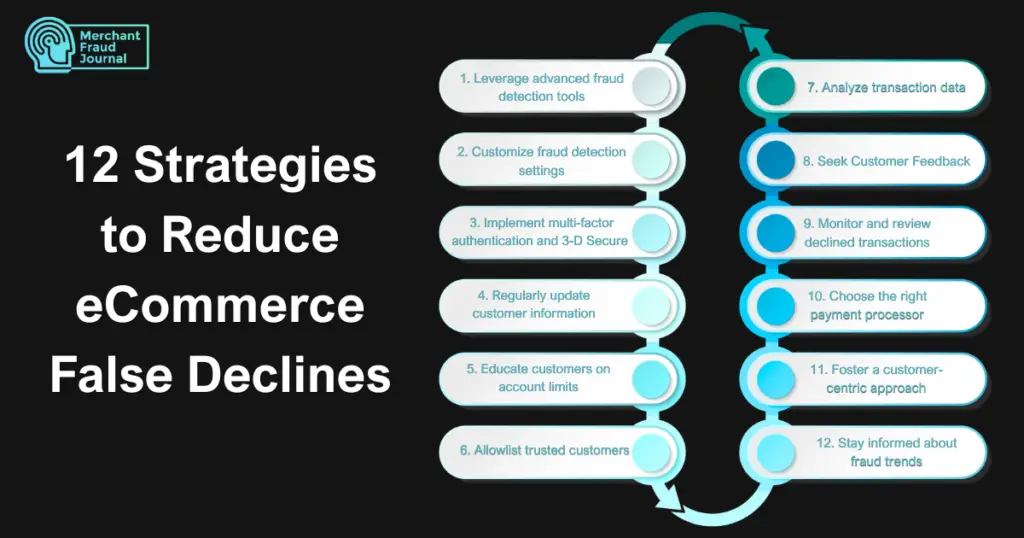

12 Strategies to Reduce eCommerce False Declines

To combat the issue of false declines, merchants must implement effective strategies that balance fraud prevention with a seamless customer experience. Here are several approaches to that help reduce eCommerce false declines:

1. Leverage advanced fraud detection tools

Investing in sophisticated fraud detection systems that utilize machine learning and artificial intelligence can significantly reduce false declines. Rather than relying on rigid, manual rules, modern eCommerce fraud protection platforms, such as Signifyd, Kount, and Riskified, analyze vast amounts of behavioral, device, and transactional data in real-time.

2. Customize fraud detection settings

Many payment processors offer customizable fraud detection settings. Merchants can reduce the likelihood of false declines by adjusting these parameters to align with the specific transaction patterns of their customer base.

Rather than relying on one-size-fits-all factory defaults, businesses can establish tailored thresholds for different risk profiles, such as treating loyal, logged-in loyalty members with more leniency than guest checkouts. Additionally, setting up a routine monthly review of transaction data allows risk teams to continuously fine-tune these rules.

3. Implement multi-factor authentication (MFA) and 3-D Secure (3DS)

Instead of outright declining transactions that appear suspicious, merchants can require additional verification through multi-factor authentication. This could involve sending a one-time password to the customer’s registered mobile number or email, adding an extra layer of security without losing the sale.

Furthermore, utilizing modern protocols like 3-D Secure (3DS) allows for frictionless authentication, meaning standard buyers rarely get interrupted while higher-risk transactions become safely vetted. This strategic friction gives legitimate customers a quick way to prove their identity, salvaging revenue that would otherwise be permanently lost to an automated rejection.

4. Regularly update customer information

Keeping customer data current is essential for minimizing false declines. Merchants should encourage customers to update their billing and shipping information regularly to ensure accuracy during transactions. This proactive approach ensures that automated fraud screenings have access to the most precise data points during real-time verification. Furthermore, maintaining an accurate database helps build a reliable historical profile for loyal shoppers.

5. Educate customers on account limits

Informing customers about any spending limits or restrictions on their accounts can help prevent declines due to exceeding these thresholds. Clear communication can enhance the shopping experience and reduce frustration.

Providing real-time notifications or pre-checkout alerts when a user nears a limit allows them to adjust their payment method before a decline occurs. This proactive approach turns a potential transaction failure into a transparent, friction-free customer milestone.

6. Allowlist trusted customers

For repeat customers with a history of legitimate transactions, merchants can implement an allowlist. This means that transactions from these customers undergo less stringent checks, reducing the chances of false declines.

To maximize effectiveness, this list should automatically sync with loyalty program data to recognize high-value, frequent buyers across multiple sales channels. However, merchants must continuously monitor these accounts using behavioral AI. Doing so ensures that sudden shifts in login locations or device fingerprints are flagged to protect the allowlist from account takeover (ATO) attacks.

7. Analyze transaction data

Regularly reviewing transaction data can help merchants identify patterns that lead to false declines.Conducting deep-dive audits into historical data allows teams to identify specific rules or fraud-scoring thresholds that are overly sensitive and acting as bottlenecks at checkout. Armed with these insights, merchants can continuously optimize their payment routing and validation parameters to maximize approval rates without increasing actual fraud risk.

8. Seek Customer Feedback

Encouraging customers to provide feedback on their experiences with false declines can offer valuable insights. This information can help merchants adjust their fraud detection measures and improve the overall customer experience.

Implementing automated post-decline surveys or reaching out via email after an order is blocked allows businesses to pinpoint exactly where their fraud rules are too aggressive. Furthermore, this direct line of communication provides a crucial opportunity to salvage the relationship, clear the misunderstanding, and successfully rescue an otherwise lost sale.

9. Monitor and review declined transactions

Merchants should regularly analyze declined transactions to identify commonalities among false declines. This practice can inform adjustments to fraud detection strategies (whether via your fraud detection analyst or automated tools) and reduce future occurrences.

Setting up a system for routine post-decision audits allows risk teams to uncover hidden patterns where valid customers were inadvertently blocked. Consistently auditing these metrics transforms historical loss into actionable data that refines overall checkout conversion rates.

10. Choose the right payment processor

Selecting a payment processor that prioritizes reducing false declines is crucial. A provider that employs advanced fraud detection techniques and offers customizable settings can make a significant difference in minimizing false declines.

Opting for a partner with extensive global banking networks ensures more accurate transaction routing and fewer algorithmic errors during checkout. Over time, this strategic alignment not only protects immediate revenue but also fosters long-term customer trust and retention.

11. Foster a customer-centric approach

Merchants should view fraud prevention as a customer experience function rather than solely a loss-prevention measure. Implementing fraud detection with a priority on customer satisfaction allows businesses to create a more positive experience. This shift in perspective ensures that security protocols remain invisible and frictionless for legitimate buyers during checkout.

12. Stay informed about fraud trends

Keeping abreast of emerging fraud tactics and trends is essential for effective fraud prevention. Merchants should regularly update their fraud detection systems to adapt to new challenges in the eCommerce landscape.

Engaging with industry networks, subscribing to cybersecurity alerts, and attending retail risk webinars can provide crucial foresight into evolving threat vectors. This continuous education allows businesses to proactively adjust their screening thresholds before new exploits impact their bottom line.

A Balanced Approach to Eliminating eCommerce False Declines

Reducing eCommerce false declines is a multifaceted challenge that requires a strategic approach. Leveraging advanced technology, customizing fraud detection settings, and fostering a customer-centric approach are key components of a successful strategy. As eCommerce continues to grow, prioritizing the reduction of false declines will be essential for long-term success in the digital marketplace.

Frequently Asked Questions

How do false declines directly impact customer retention?

When a shopper's payment is falsely rejected, it causes immediate frustration, embarrassment, and inconvenience at checkout. Studies show that nearly half of these insulted consumers will permanently abandon the brand and take their business elsewhere.

What is the most common technical reason for a false decline?

The primary driver is the use of rigid, legacy rules-based fraud systems that reject orders based on isolated discrepancies. For example, a system might automatically block an order simply because the shipping address does not match the billing address.

How does communication with issuing banks reduce false declines?

Sharing enhanced transaction data, like device indicators and customer history, directly with issuing banks builds greater processing trust. When banks receive this rich data context, they are far less likely to trigger a false decline on their end.

Charity Amancio

Charity Amancio specializes in SaaS solutions for global eCommerce businesses, including payments and risk management applications. She bridges the gap between technology and merchant needs, offering practical perspectives on the tools shaping eCommerce. Her insights appear regularly in B2B publications covering the digital commerce space.